Short Term Cash Forecasting: Quick Wins for Cash Visibility

Most businesses discover cash problems too late-when they’re already in crisis. Short term cash forecasting gives you the visibility to spot gaps weeks or months ahead, so you can act before trouble strikes.

This guide walks you through proven quick wins that deliver immediate results. You’ll learn how to implement rolling forecasts, automate tracking, and monitor the metrics that matter most to your bottom line.

Why Cash Forecasting Matters

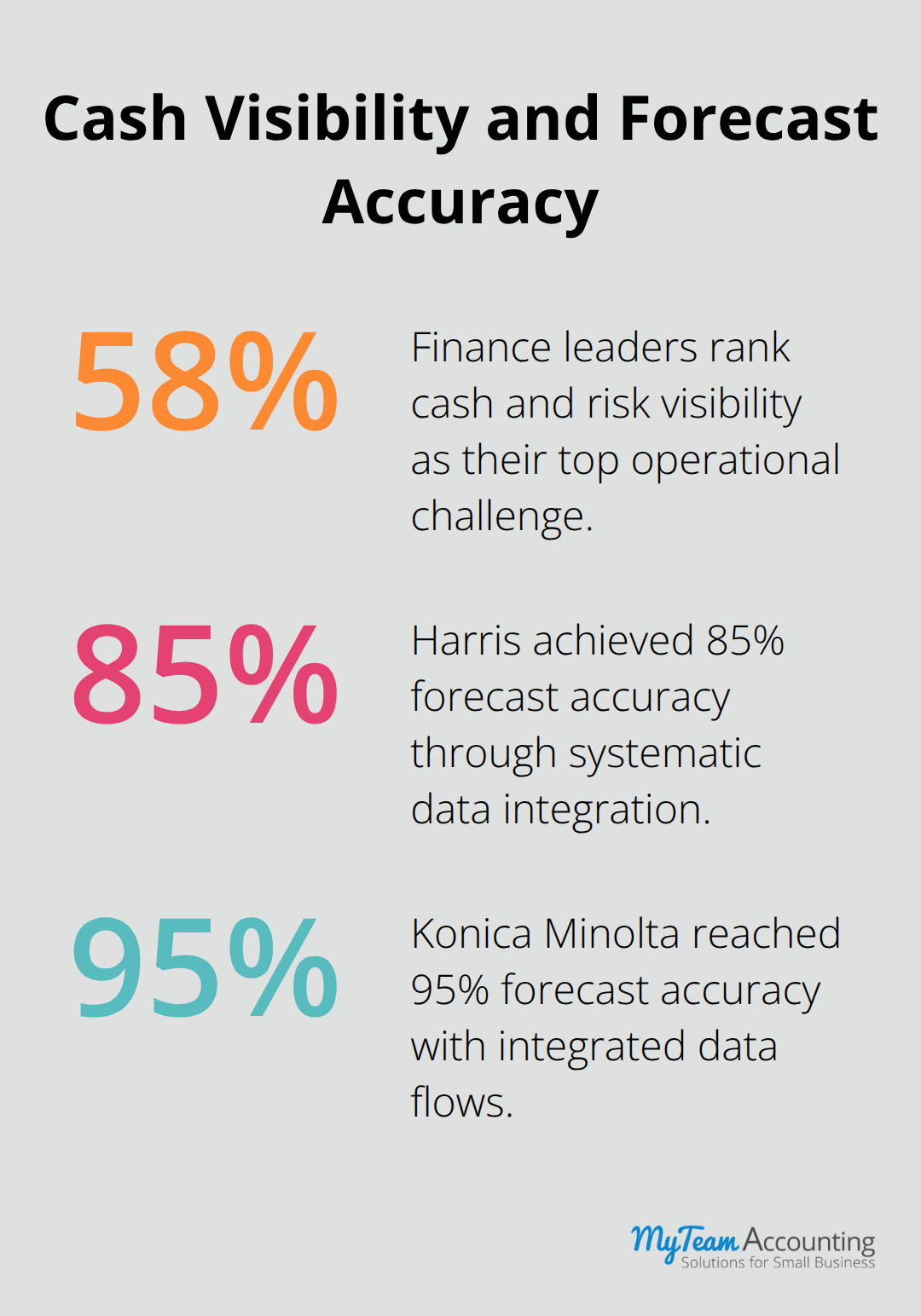

Cash forecasting stops being optional the moment your business scales beyond a handful of transactions per week. Deloitte’s 2024 Global Treasury Survey found that 58% of finance leaders rank visibility into cash and risk exposures as their top operational challenge, yet most still rely on spreadsheets and manual bank checks. Short-term forecasting solves this by showing you exactly where cash gaps will appear seven to ninety days out, giving you time to adjust spending, delay non-critical payments, or secure financing before a shortfall becomes a crisis.

Spot problems before they paralyze operations

Most cash emergencies aren’t truly emergencies-they’re foreseeable gaps that nobody saw coming because nobody was looking. A business with three weeks of payroll runway and a major customer payment due in ten days doesn’t have a revenue problem; it has a timing problem that a rolling forecast catches instantly. When you forecast daily or weekly cash positions out thirty to sixty days, you spot the exact date when your balance dips below your minimum operating threshold. This isn’t theoretical; it’s the difference between having time to invoice faster, negotiate payment terms, or tap a line of credit versus scrambling at the last minute with limited options. Real-time visibility into accounts receivable and accounts payable statuses feeds directly into these forecasts, so you track what actually moves through your system and when money will actually land in your account.

Make capital allocation decisions with confidence

When you know your cash position for the next sixty days with accuracy above 85%, spending decisions shift from hope-based to data-based. You can confidently approve an equipment purchase because you’ve already accounted for payroll, taxes, and supplier payments across that window. You stop hoarding cash unnecessarily or, worse, borrowing money while idle funds sit in low-yield accounts. Scenario planning amplifies this further-test what happens if your top customer delays payment by two weeks, or if seasonal demand dips harder than expected. This stress-testing reveals which decisions are truly safe and which ones create hidden risk. The best forecasting platforms integrate directly with your accounting software, pulling actual invoice schedules and payment histories so your scenarios rest on real data, not assumptions.

Move from spreadsheets to actionable intelligence

Spreadsheets create blind spots because they capture only a snapshot in time. You update them weekly or monthly, but cash moves daily-invoices land, payments process, and your forecast becomes stale within hours. Modern accounting software eliminates this lag (QuickBooks and Xero both offer real-time data feeds) and connects directly to your bank accounts, so your forecast updates automatically as transactions clear. This continuous refresh means you catch anomalies fast: a customer who typically pays in thirty days suddenly stretches to forty-five, or a seasonal spike arrives earlier than expected. You respond to what’s actually happening, not what you assumed would happen.

The next section explores the specific quick wins that deliver these results without requiring a complete system overhaul.

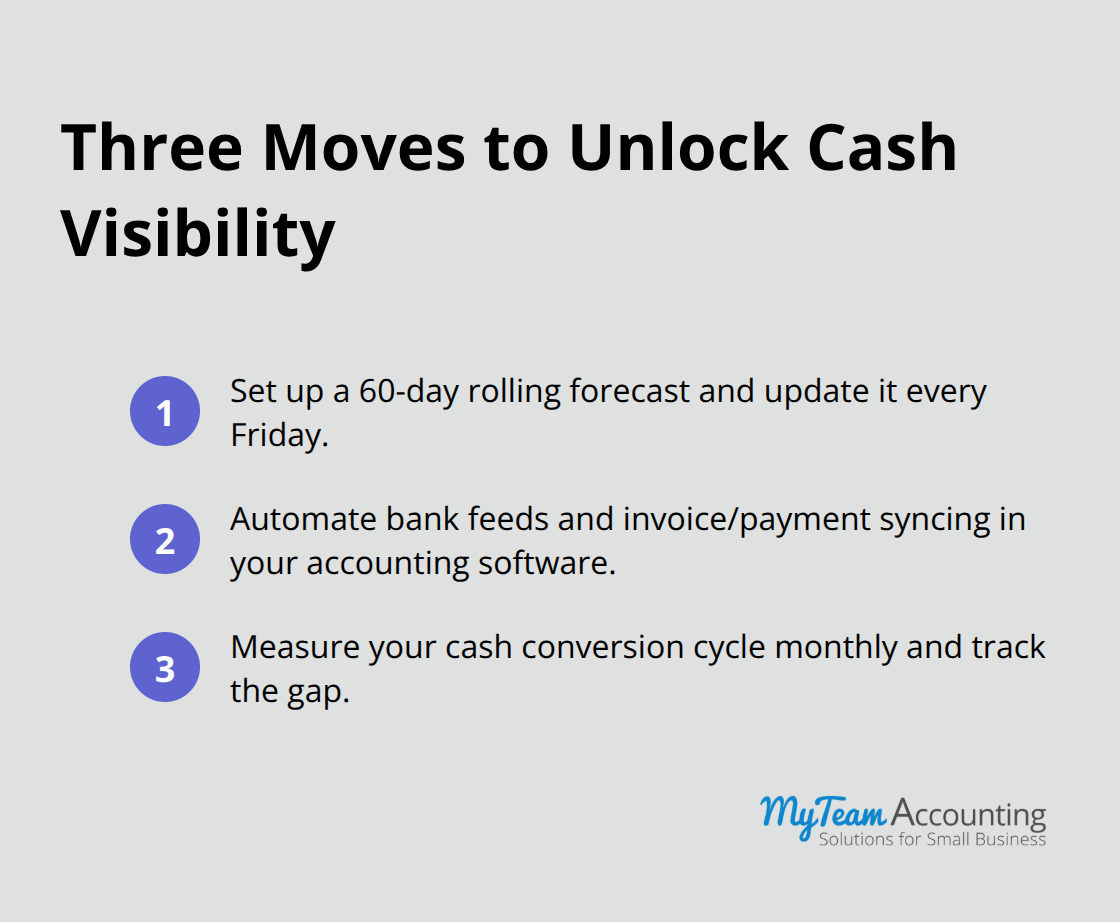

Three Moves That Unlock Cash Visibility in Weeks

Set Up Rolling Forecasts with Discipline

Rolling forecasts demand discipline, not complexity. Start by pulling your last ninety days of actual bank transactions, invoice dates, and payment clearing times from your accounting software. Then map the next sixty days forward: every known invoice due, every paycheck scheduled, every tax payment or loan installment already locked in. Update this forecast every Friday with the prior week’s actuals and extend it another week forward, so you always have sixty days of visibility. Most businesses discover within two weeks that their cash position dips lower than they assumed, exposing a timing gap nobody saw in monthly financial statements. That gap becomes your earliest warning signal.

The discipline matters more than the tool-spreadsheets work if you update them religiously, though cloud accounting platforms like QuickBooks or Xero eliminate the manual step entirely by pulling real transactions automatically. Assign one person ownership of this forecast; rotating responsibility kills the process because assumptions get lost and updates skip. Test your forecast accuracy after thirty days by comparing predicted balances against actual bank statements.

Automate Invoice and Payment Tracking

Automation of invoice and payment tracking stops the bleeding immediately. Connect your accounting software directly to your bank accounts so transactions appear in real time rather than clearing through manual bank feeds three days later. This three-day lag alone explains why businesses overdraft despite having cash on the way-the forecast shows no problem, but the bank sees an empty account because deposits haven’t posted yet.

Next, configure your accounting software to flag invoices unpaid beyond their due date and payments scheduled before cash actually lands. Most platforms offer conditional alerts: notify the owner when accounts receivable exceeds a threshold, or when cash projected to arrive in the next seven days falls below operating expenses. These alerts prevent the crisis moment where payroll processes but a major customer invoice hasn’t cleared.

Measure Your Cash Conversion Cycle

Establish cash conversion cycles by measuring the actual days between when you pay suppliers and when customers pay you. A thirty-day payment cycle to suppliers combined with a forty-five-day collection cycle creates a fifteen-day cash gap that must be funded somehow. Know this number precisely for your business; calculate it monthly and track trends. If the gap widens, you’ve found where cash pressure originates.

Some businesses solve this through early payment discounts to suppliers or by invoicing customers on net-fifteen terms instead of net-thirty. Others use supplier financing or receivables acceleration programs to compress the gap. The point is you cannot fix what you do not measure, and most businesses operate blind to their actual cash conversion cycle because they never bothered to calculate it. Once you understand this cycle, you position yourself to move beyond reactive cash management into the strategic forecasting that separates stable businesses from those constantly fighting for liquidity.

Tools That Turn Data Into Decisions

Configure Accounting Software as a Forecasting Engine

Real-time accounting software forms the backbone of effective forecasting, but only if you configure it correctly. QuickBooks and Xero both pull bank transactions automatically, which eliminates the three-to-five-day lag that kills forecast accuracy. Most businesses treat these platforms as record-keepers rather than forecasting engines. Instead, connect your bank accounts and configure conditional alerts that trigger when accounts receivable ages past forty-five days or when projected cash for the next fourteen days falls below your minimum operating balance. These alerts should land in your inbox or your accounting software dashboard every morning, not buried in a weekly report. Enterprises like Harris achieved 85% forecast accuracy and Konica Minolta reached 95% accuracy through systematic data integration. The pattern across high-performing forecasters remains identical: they connect everything-bank feeds, invoice schedules, payment calendars, payroll cycles-into one system and let automation flag anomalies before humans miss them. This approach helps you interpret data so you can make decisions that strengthen your forecasting capability.

Test Multiple Scenarios to Expose Hidden Risk

Scenario planning separates businesses that merely forecast from those that actually control cash. Load your sixty-day rolling forecast into a simple spreadsheet or dedicated forecasting tool, then test what happens under stress. Delay your largest customer payment by two weeks, reduce sales revenue by twenty percent, or push a major vendor payment forward by ten days. Run these scenarios monthly, not just once. Your cash conversion cycle changes seasonally, customer payment behavior shifts, and supplier terms evolve. A business that stress-tested its forecast in January but not June gets blindsided when summer slowdowns compress cash flow differently than expected.

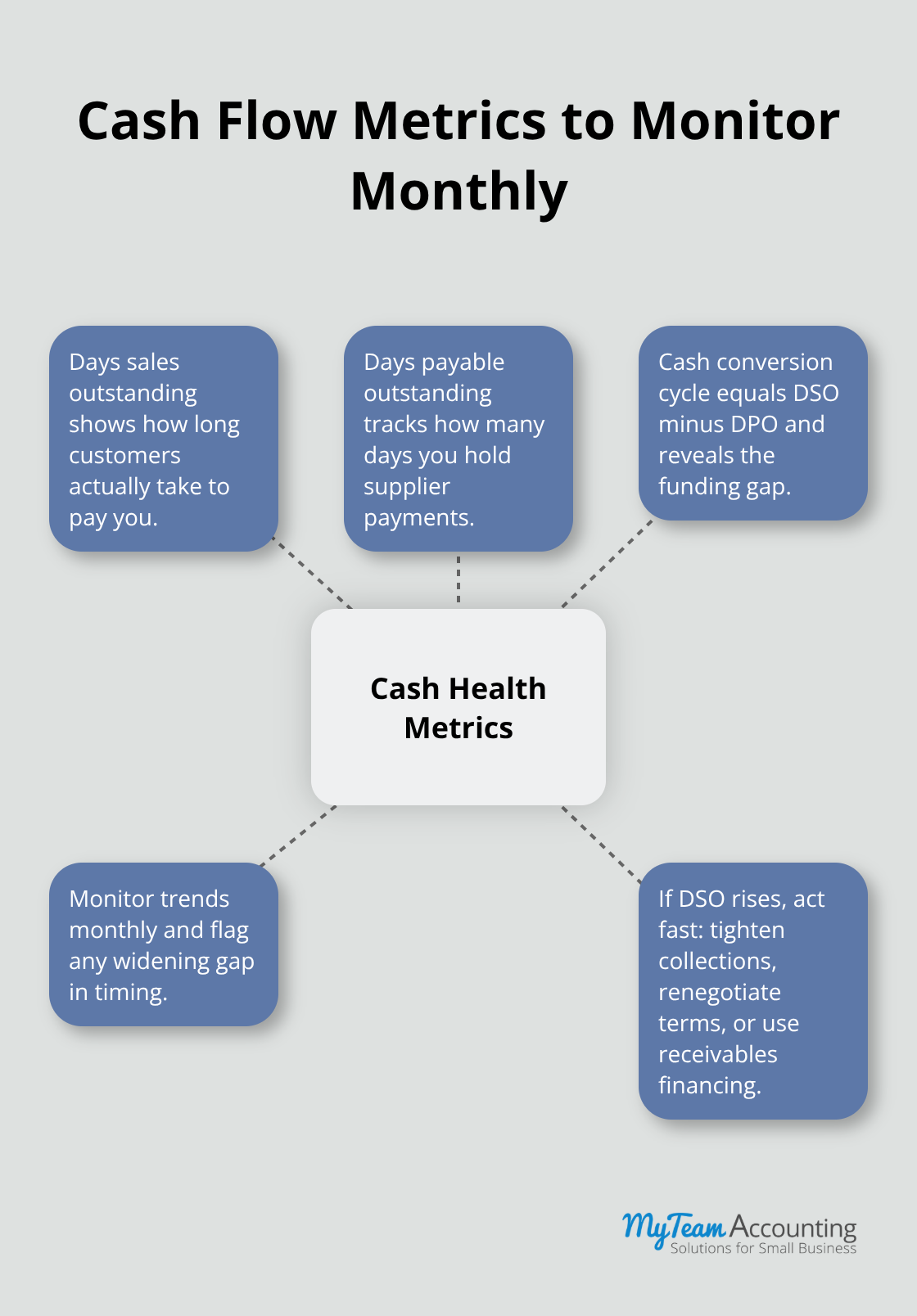

Monitor the Three Metrics That Matter Most

Track three core metrics religiously: days sales outstanding (how many days until customers actually pay you), days payable outstanding (how many days you hold supplier payments), and the cash conversion cycle itself (DSO minus DPO). Monitor these monthly and flag any trend that widens the gap. When DSO creeps from thirty-five to forty-five days, your cash pressure intensifies immediately, even if revenue stays flat.

Final Thoughts

Short-term cash forecasting transforms how you manage liquidity, but only if you move from planning to action. Start with rolling forecasts, automate what you can, and measure your cash conversion cycle-within weeks, you’ll spot timing gaps that monthly financial statements hide and catch payment delays before they become crises. These steps eliminate most cash surprises because you stop flying blind and start making spending decisions backed on actual cash visibility.

Pull your last ninety days of transactions and map the next sixty days forward with every known invoice, paycheck, and payment obligation. Assign one person to update this forecast every Friday and configure alerts in your accounting software to flag when accounts receivable ages or when projected cash dips below your minimum operating threshold. Connect your bank accounts directly to your accounting software so transactions appear in real time, then calculate your actual cash conversion cycle by measuring days between when you pay suppliers and when customers pay you.

Stress-test your forecast monthly by modeling what happens if your largest customer delays payment or seasonal demand shifts (this scenario planning exposes hidden risks before they paralyze operations). Businesses that forecast accurately reduce idle cash, avoid unnecessary borrowing, and free their owners from constant financial anxiety. Discover how modern accounting software can help you implement these practices and transform your cash management approach.