Top Accounting Mistakes Small Business Owners Make (and How to Avoid Them)

Many small business owners focus on growth and sales while overlooking the financial foundation that keeps their company stable. Accounting mistakes-from poor cash flow management to disorganized records-can quietly drain profits and create costly compliance problems.

The good news is that most of these errors are preventable. This guide walks you through the top accounting mistakes small business owners make and gives you practical accounting tips to avoid them, so you can protect your business finances and maintain accurate financial records.

Mismanaging Cash Flow and Invoicing

Why Your Cash Isn’t Matching Your Records

Cash flow mismanagement destroys more small businesses than poor sales ever will. The problem isn’t that owners don’t care about money-it’s that they confuse invoices sent with cash received. You can have a profitable business on paper and still run out of money to pay employees. This happens because most small business owners treat accounts receivable like a passive process when it demands constant, aggressive attention.

Your invoices won’t collect themselves. When you send an invoice and forget about it, you essentially give your customer a free loan. The longer an invoice sits unpaid, the harder it becomes to collect. Instead of hoping customers pay on time, implement a system where you follow up within three days of sending an invoice, then again at day seven if unpaid, and finally before day thirty. This isn’t rude-this is business. Customers expect this rhythm.

The Hidden Cost of Skipped Reconciliations

Many owners fail to reconcile their bank statements monthly, which means discrepancies between what they think they have and what’s actually in the account can hide for weeks. Unreconciled accounts mask errors, failed transactions, and even fraudulent activity. You should spend fifteen minutes every month matching your accounting software to your bank statement. If something doesn’t match, investigate immediately. A missing deposit or duplicate charge compounds quickly.

The core issue is that most owners treat bookkeeping as a month-end task instead of a daily habit. Real-time expense tracking and invoice management prevent the chaos of playing catch-up. When you categorize transactions and attach receipts as they happen, you know your actual cash position at any moment.

Cash Flow Forecasting Requires Current Records

This matters because cash flow forecasting-projecting inflows and outflows over the next thirty, sixty, or ninety days-only works if your records are current. Without it, you can’t tell whether you’ll have enough cash to cover payroll or vendor payments. Many owners also negotiate poor payment terms with customers, allowing thirty or sixty days to pay while they pay suppliers in ten days. This creates a cash gap that strangles growth.

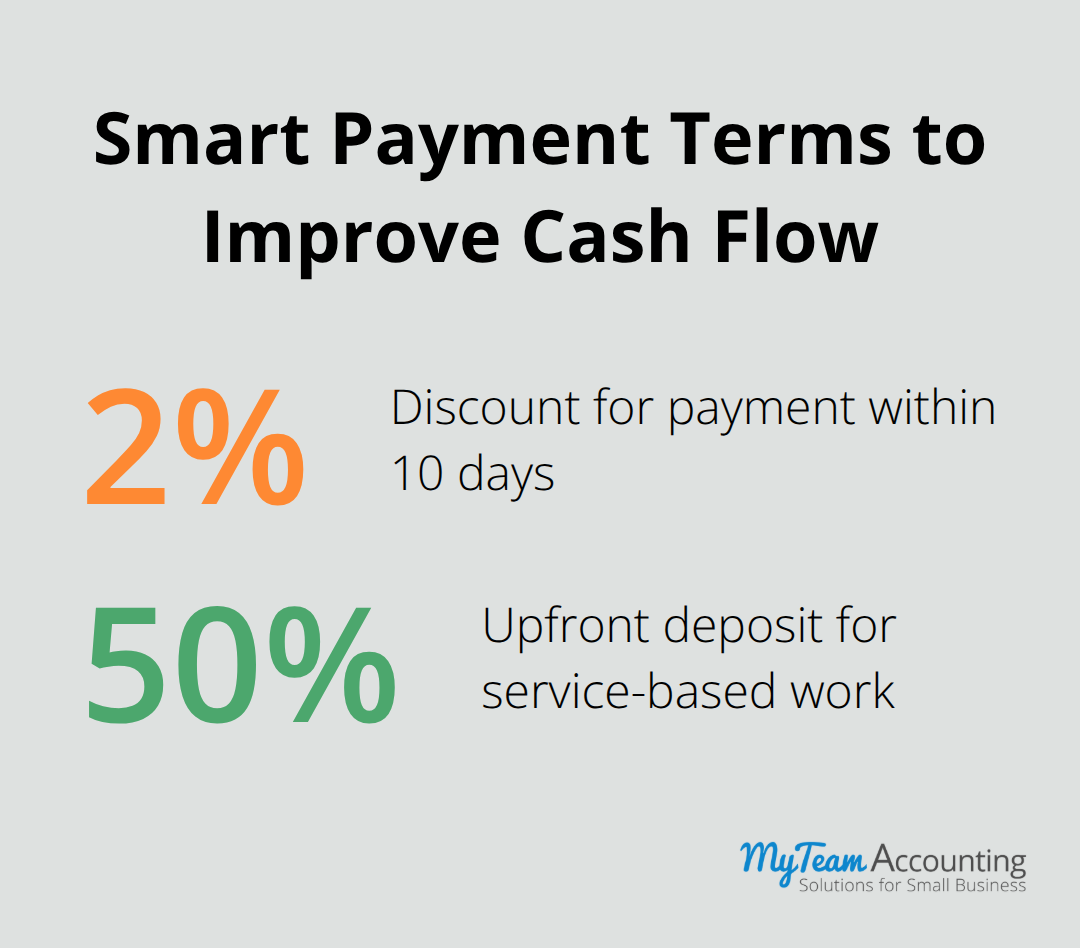

Offer a two percent discount for payment within ten days, or require fifty percent upfront for service-based work. On the vendor side, use payment terms negotiation to align your cash inflows and outflows.

Common Tax and Compliance Errors That Cost Small Businesses Thousands

The moment you hire your first worker or miss a quarterly tax payment, you enter territory where mistakes carry real financial and legal consequences. Many small business owners treat tax compliance as a once-a-year exercise, but the IRS and state agencies operate on schedules that demand attention throughout the year. Misclassifying a worker as an independent contractor instead of an employee can trigger back taxes, penalties, and payroll tax liabilities that dwarf the original salary savings.

Worker Classification: Get It Right From Day One

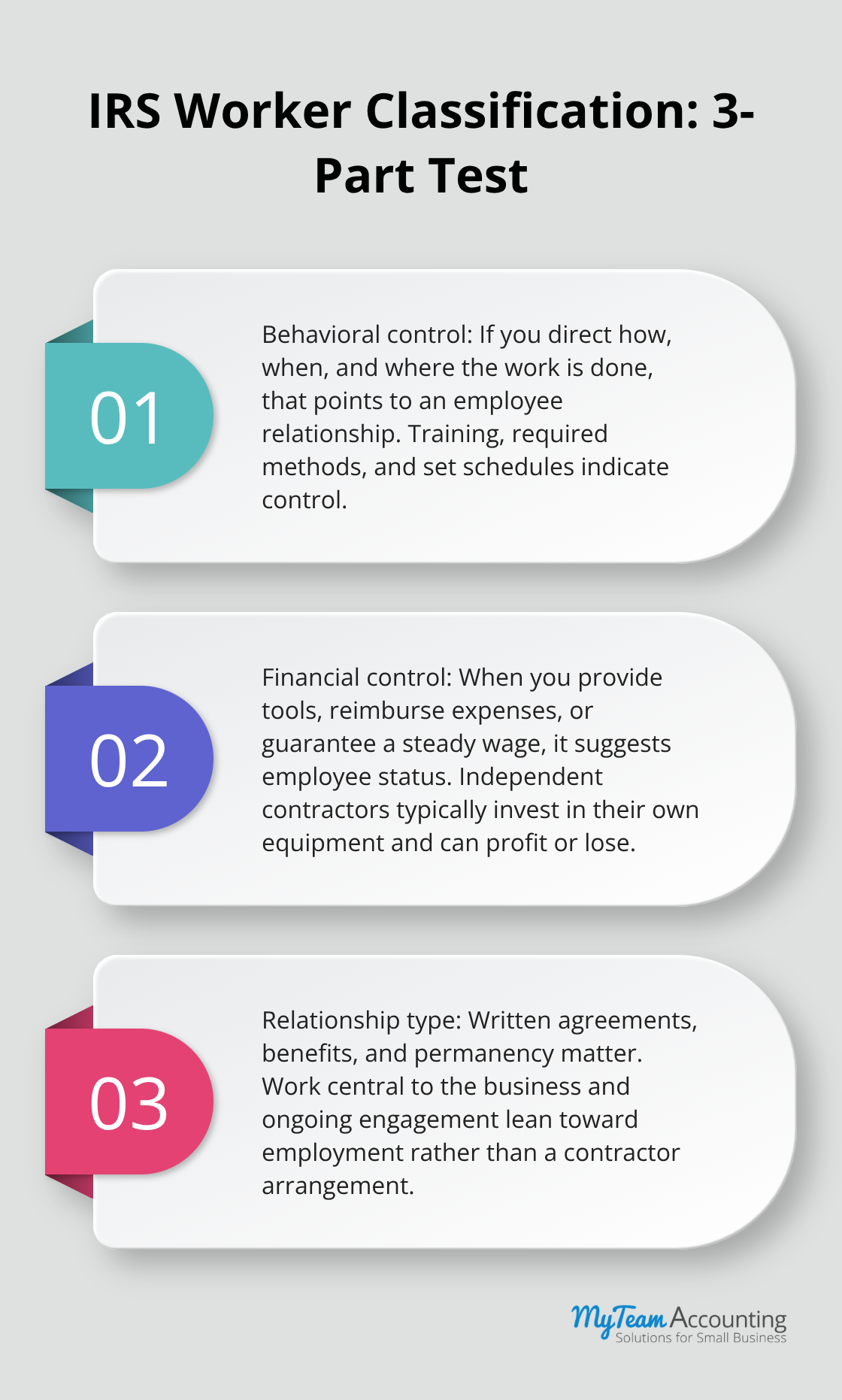

The IRS uses a three-part test to determine worker status: behavioral control, financial control, and relationship type. If you pay someone a salary, provide equipment, set their schedule, and control how they work, they are an employee. A contractor should manage their own tools, work for multiple clients, and maintain independence. Document this classification in writing before you pay anyone.

Collect a completed W-9 form from every 1099 contractor before cutting the first check, not after tax season when chaos erupts. This single document protects you from penalties and prevents last-minute scrambling when filing deadlines arrive.

Quarterly Taxes Aren’t Optional

Quarterly estimated tax payments are mandatory for business owners, yet many treat them as optional suggestions. If you earn net profit above four hundred dollars, you owe estimated taxes every quarter to the IRS and likely to your state. Missing even one quarterly payment triggers penalties and interest that compound through the year. The IRS calculates these based on your prior year income or current year projections, and underpayment penalties run around five percent annually.

Set calendar reminders for April 15th, June 15th, September 15th, and January 15th. Calculate your estimated liability now, not in March. Work with a CPA or tax advisor in January to determine your quarterly amount so you know exactly what to set aside. Many owners fail to do this and then scramble when the bill arrives. Pay electronically through the IRS website or your bank to create an immediate paper trail. A two-minute payment today prevents weeks of stress and hundreds in penalties later.

Commingling Finances Destroys Legal Protection

Separating personal and business finances isn’t administrative busy work. It’s the difference between protecting your personal assets and exposing them to liability. When you run business expenses through your personal account or deposit customer payments into your personal checking, you erase the legal boundary that protects you as a business owner. Courts look at this commingling during litigation or claims against your business, and if they find your finances mixed together, they can pierce your corporate veil and hold you personally liable.

Open a dedicated business bank account immediately and use only that account for all business transactions. Get a separate business credit card and use it exclusively for business purchases. Reimburse yourself formally when you spend personal money on business needs. This creates clear documentation and maintains the separation that courts recognize. If you operate an LLC or corporation, this separation is non-negotiable. It costs nothing to set up and everything to ignore.

These tax and compliance errors demand immediate attention, but they pale in comparison to the chaos that disorganized record-keeping creates across your entire financial operation.

Disorganized Records Destroy Financial Clarity

Most small business owners don’t realize that disorganized bookkeeping costs real money. When your financial records lack consistency, you miss deductions, overpay taxes, fail to catch fraud, and make decisions based on incomplete or incorrect data. The real cost isn’t the time spent organizing; it’s the opportunities lost and the penalties incurred because you can’t see what’s actually happening in your business. Businesses using cloud-based accounting software make better financial decisions and spend less time on month-end close procedures than those relying on spreadsheets or manual entry. This gap matters because disorganization compounds. One uncategorized transaction becomes ten, then fifty, then your entire month-end close takes three weeks instead of two days. At that point, you’re making decisions on stale data.

Establish a Clear Chart of Accounts

Start with a chart of accounts tailored to your business instead of relying on vague categories like miscellaneous or other. Create specific accounts that match how you actually operate. If you run both online and in-person sales, separate them. If you have multiple revenue streams, track each one independently. This structure lets you see which parts of your business are profitable and where to invest next.

Implement Daily Categorization and Receipt Tracking

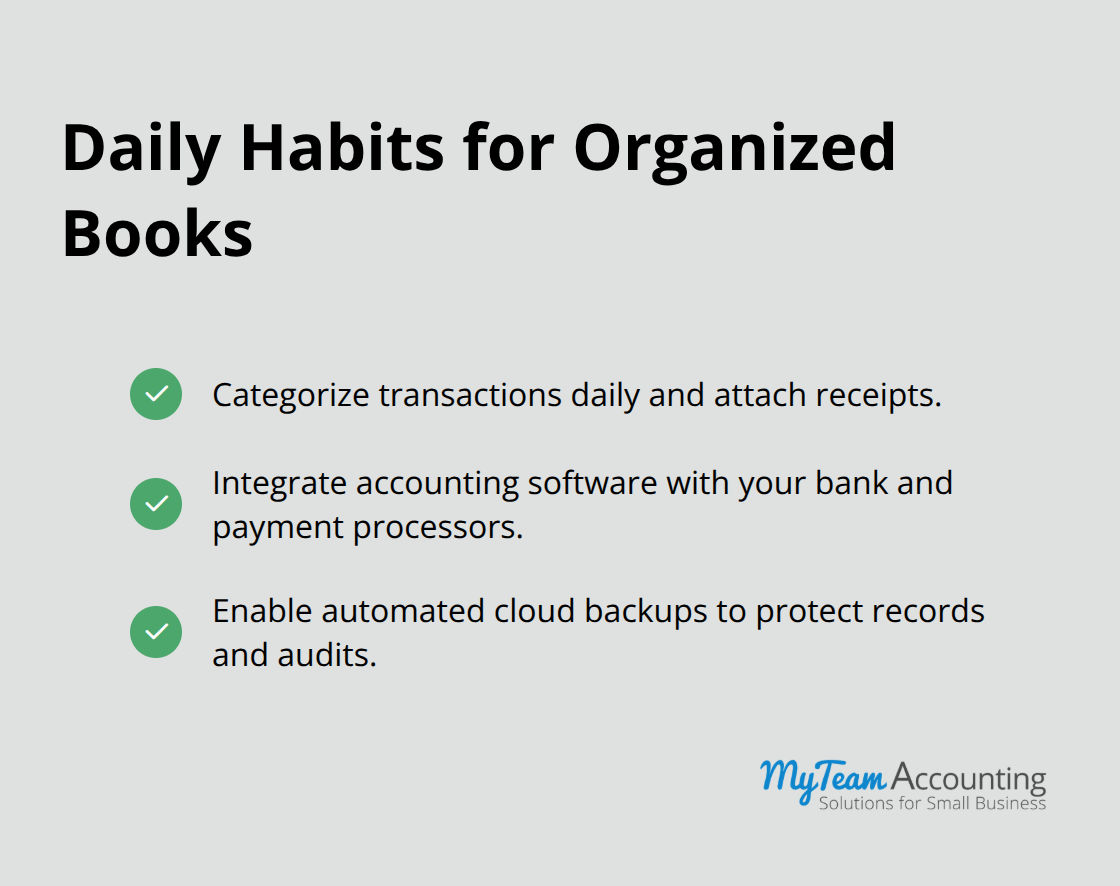

Categorize every transaction the day it happens-not weekly, not monthly. Attach receipts immediately through your accounting software rather than collecting them in a shoebox. Set rules for recurring expenses so subscriptions and regular vendor payments categorize automatically. This daily discipline takes fifteen minutes and prevents the chaos of reconciliation later. Most small business owners who claim bookkeeping takes too long are actually spending hours fixing problems created by weeks of procrastination.

Connect Your Accounting System to Your Bank

Your accounting system must integrate with your bank, payment processors, and invoicing tools. Spreadsheets and disconnected software require manual entry at every step, which introduces errors and wastes time. Cloud-based accounting platforms automatically pull transactions from your bank account, match them to invoices, and flag discrepancies. This automation catches duplicate charges, missing deposits, and timing mismatches before they become problems. The platform also maintains a complete audit trail showing who entered what and when, which protects you during tax reviews or disputes.

Integration also means your accountant or bookkeeper can access current data without you manually exporting files or sending statements. They see real-time transactions, categorization, and cash position, which lets them spot issues early and provide better guidance.

Protect Your Data With Automated Backups

Implement automatic daily backups stored in the cloud. Data loss from hardware failure, ransomware, or accidental deletion can destroy your financial records and compliance documentation.

These three practices-consistent daily categorization, integrated software, and automated backups-transform bookkeeping from a burden into a reliable system that gives you accurate financial clarity every single day.

Final Thoughts

The accounting mistakes outlined in this guide stem from one core problem: treating finances as a periodic task rather than an ongoing operating habit. Small business owners prioritize immediate growth over the financial infrastructure that sustains it, yet preventing these errors requires only consistency and the right systems. Start by implementing the accounting tips covered here-separate your personal and business finances completely, reconcile your bank statements monthly, categorize transactions daily, and set calendar reminders for quarterly tax payments.

As your business grows, the complexity of managing finances alone increases exponentially. A qualified bookkeeper or accountant becomes invaluable not just for compliance, but for strategic insight. They catch errors before they compound, identify tax-saving opportunities you’d miss, and free you to focus on what you do best. Consider this investment in professional support as insurance against costly mistakes and as a catalyst for better financial decisions.

Your next step is simple: choose one accounting mistake from this guide that resonates most with your current situation and fix it this week. If your records lack organization, implement cloud-based accounting software with bank integration to transform your financial records into a reliable foundation for decision-making. Small actions compound into systems that protect your business finances and keep you audit-ready year-round.