Dynamic Cash Flow Forecasting: Anticipate Shifts and Opportunities

Many businesses struggle with unpredictable cash flow, missing opportunities and facing unexpected shortfalls. Dynamic cash flow forecasting transforms this challenge by giving you visibility into your financial future.

With accurate forecasts, you can anticipate shifts in revenue and expenses before they impact your operations. This guide walks you through proven strategies to build a forecasting system that strengthens your financial planning and supports sustainable growth.

Why Cash Flow Forecasting Matters

Cash flow forecasting stops being optional the moment your business scales beyond a single revenue stream. Most growing companies fail not because they lack profits on paper, but because cash runs dry before invoices get paid. A SaaS company with $500,000 in monthly recurring revenue can still face a liquidity crisis if 60-day payment terms delay cash by two months while payroll hits every other week. This gap between when you earn revenue and when you actually receive it destroys businesses that ignore it. The solution is straightforward: forecast with precision, update weekly, and tie those forecasts directly to your hiring and spending decisions. Companies that implement rolling 12- to 18-month projections updated regularly catch revenue problems months before they become crises. Without this visibility, you operate blind, making investment decisions on outdated information and discovering cash shortfalls only when vendors demand payment or payroll cannot clear.

Anticipate Revenue Timing Before Cash Dries Up

Dynamic forecasting requires you to model exactly when money arrives, not just whether it arrives. A $100,000 contract with net-60 terms does not generate usable cash for two months, yet most founders treat it as immediate revenue. Real-time data integration from Stripe, QuickBooks, or your bank APIs removes guesswork-auto-refreshing forecasts as payments actually post. Track days cash on hand: divide current cash by average daily burn rate. If you have $200,000 cash and $10,000 daily burn, you have 20 days of runway. That number forces honest conversations about when fundraising must happen. Seasonal fluctuations matter enormously. A retail business seeing 40 percent of annual revenue in November and December must carry sufficient cash reserves in October or face collapse. Try targeting a cash buffer at 10 to 15 percent of total monthly outflows, with higher reserves if your sales cycle exceeds 90 days or if customer concentration risk is high. Without this buffer, a single lost deal or delayed payment becomes existential.

Separate Fixed Costs from Variable Spending to Control Burn

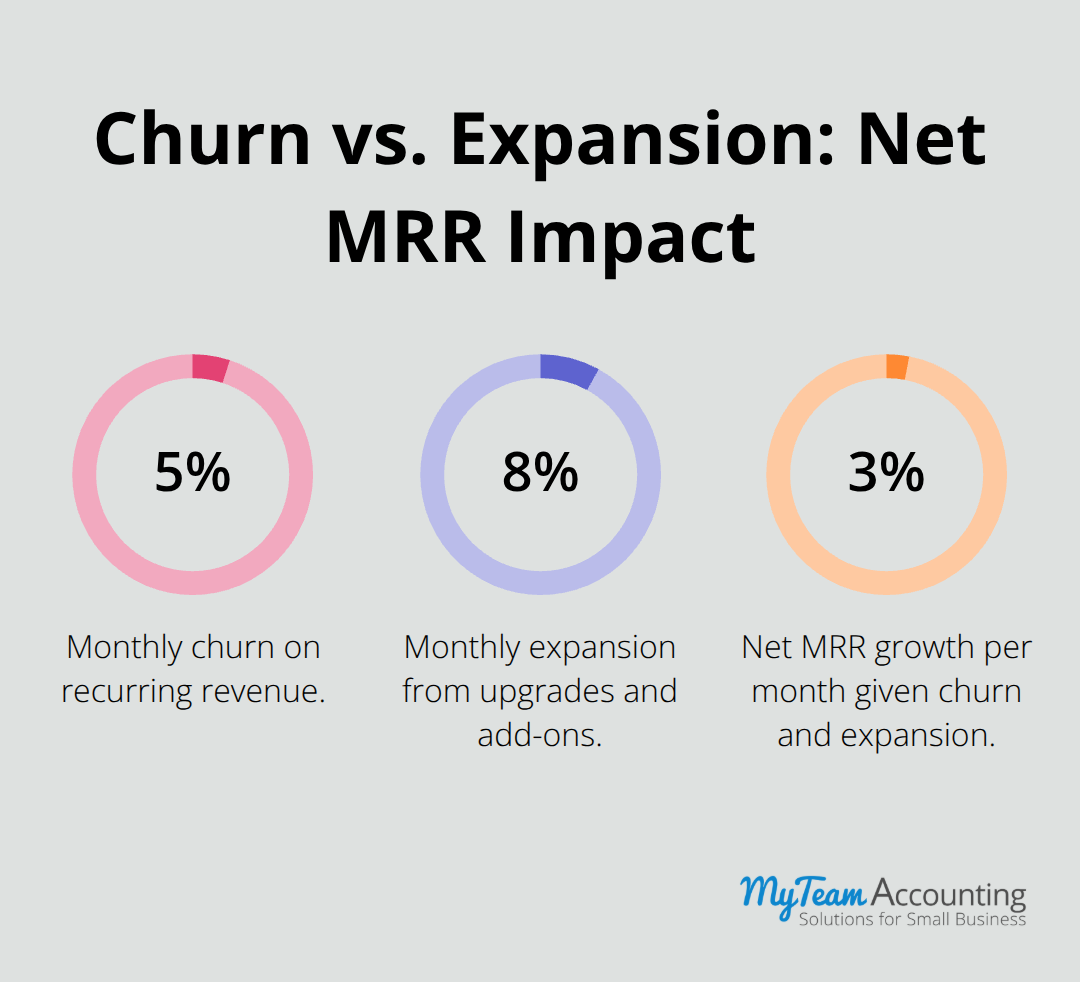

Most forecasts fail because founders lump all expenses together. A $150,000 annual salary adds roughly $12,500 to monthly burn regardless of revenue, while marketing spend flexes with growth plans. When you separate these, you see exactly how hiring decisions impact runway. A new salesperson’s $80,000 salary plus $40,000 commission budget extends burn by $10,000 monthly but should generate pipeline velocity that justifies the expense. Model churn and expansion revenue explicitly: if your company has $500,000 MRR but loses 5 percent to churn while gaining 8 percent from upgrades, net growth is 3 percent monthly, which fundamentally changes staffing capacity and cash needs.

The next chapter explores the specific components you need to track to build a forecasting system that actually works.

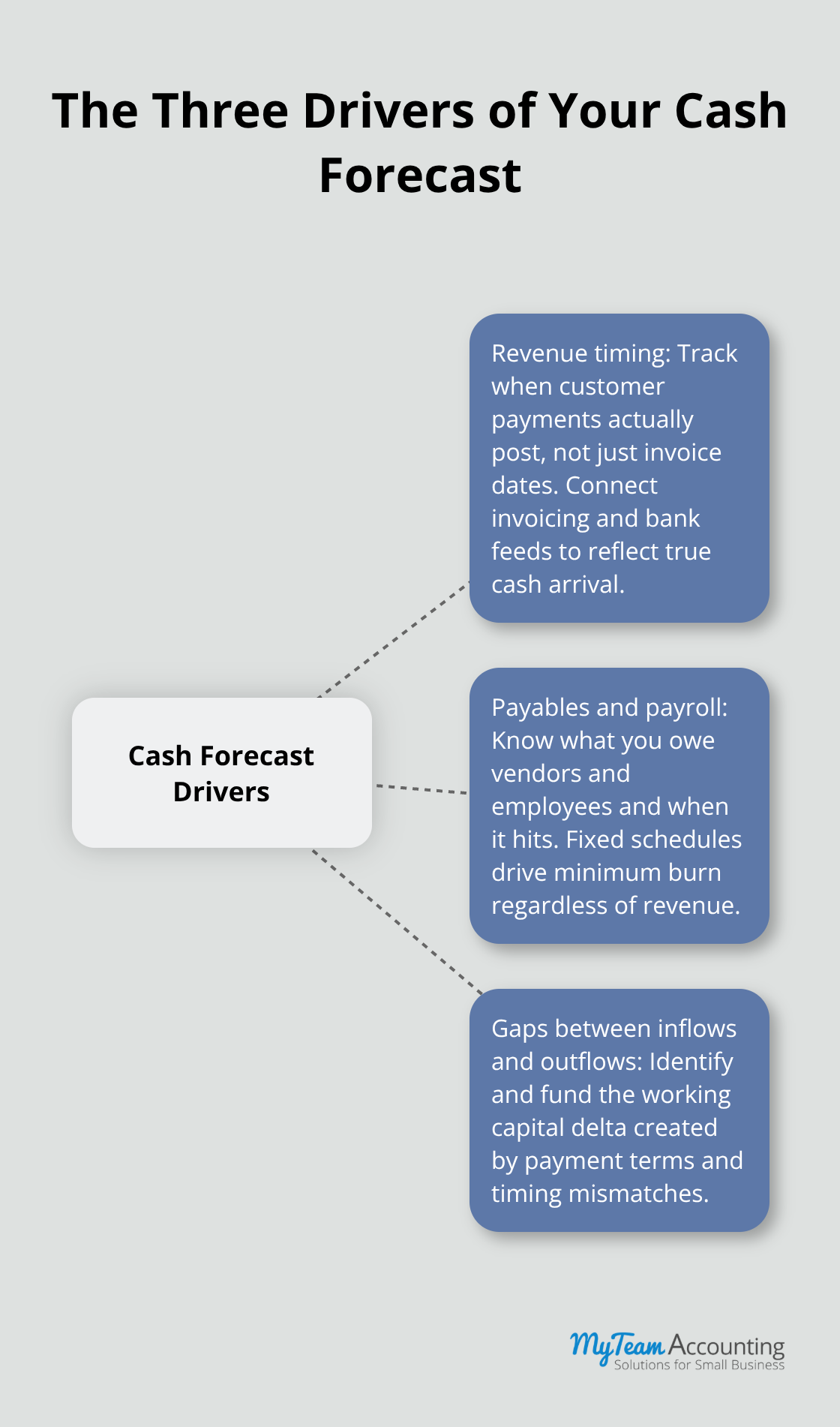

What Data Points Actually Drive Your Cash Forecast

Building a forecast that predicts reality requires brutal honesty about which numbers matter and which distract you. Most founders obsess over vanity metrics while ignoring the three data points that determine whether you survive the next quarter: when revenue actually arrives, what you owe vendors and employees, and the gaps between them.

Revenue Timing Determines Cash Reality

Start with revenue timing, not revenue recognition. Your accounting software shows $500,000 in sales this month, but that means nothing for cash forecasting if half those contracts have net-30 or net-60 terms. Connect your invoicing system directly to your bank feed and QuickBooks to track when payments actually post, not when you issue invoices. Pipeline probability weighting sharpens this further: assign realistic conversion rates to each deal stage based on your historical data, then weight them accordingly. A $200,000 deal in proposal stage with a 20 percent historical close rate contributes $40,000 to your cash forecast, not the full amount.

For SaaS and subscription businesses, model churn explicitly as a percentage reduction each month rather than treating recurring revenue as guaranteed. If you have $100,000 MRR and lose 3 percent monthly to churn, that is $3,000 gone before expansion revenue or new customer acquisition arrives. Expansion revenue from upgrades and add-ons often offsets churn but only if you track it separately. Track accounts receivable aging reports weekly, not monthly. Segment customers into payment reliability tiers and calculate average collection time for each, then factor in realistic delays. A customer who consistently pays on day 45 despite net-30 terms needs a 45-day adjustment in your forecast, not a 30-day one.

Fixed and Variable Costs Require Different Logic

On the expense side, itemize every fixed and variable cost separately and update this monthly. Fixed costs like rent, insurance, and base salaries do not change when revenue dips, so they drive your minimum monthly burn. Variable costs like payment processing fees, shipping, or hourly contractor rates scale with revenue but require different forecasting logic. Model payroll with precision: include base salaries, taxes, benefits, and any commission structures, then forecast hiring additions tied to revenue milestones rather than arbitrary dates.

One common forecasting failure is ignoring payment terms with vendors. If you negotiate net-60 terms with suppliers but your customers pay you net-45, that 15-day gap creates a working capital hole you must fund with cash reserves. Conversely, negotiating shorter payment terms with vendors or requesting early payment discounts can improve cash conversion cycles dramatically. Track capital expenditures separately because they hit cash immediately but do not appear in operating expense forecasts. A $50,000 software implementation or equipment purchase in quarter two must be reserved for in advance, not discovered when the invoice arrives.

Real-Time Data Feeds Replace Static Forecasts

Use real-time data feeds from your bank, payment processors like Stripe, and accounting software to refresh forecasts weekly. Static monthly forecasts become obsolete within days when you operate at scale. Automated integrations eliminate manual data entry errors and reveal cash position changes before they become problems. You adjust spending or accelerate collections before a shortfall occurs, rather than discovering the problem after it has already damaged your operations.

The next chapter examines how to structure your forecasting cadence and review process to keep these data points current and actionable.

How Often Should You Actually Update Your Forecast

Weekly Updates Catch Problems Before They Become Crises

Weekly forecast updates are non-negotiable if you want accuracy that actually informs decisions. Monthly reviews discover cash shortfalls after they have already damaged your operations, while weekly updates catch problems when you still have time to act. Set a specific day each week-Tuesday morning works well because it follows weekend reflections-and spend 30 minutes pulling fresh data from your bank feeds, payment processor dashboards, and accounting software. This cadence matches how fast your business actually moves. A major customer cancellation on Wednesday should shift your forecast by Thursday, not wait until next month’s review cycle.

Establish clear ownership: assign one person responsibility for running the forecast, whether that is your CFO, finance manager, or a fractional CFO service. That person owns the accuracy and communicates variance between forecasted and actual cash weekly to leadership. Without clear ownership, forecasts drift into irrelevance as data becomes stale and assumptions go unchallenged.

Track Variance to Recalibrate Your Assumptions

Track forecast accuracy relentlessly. Each month, compare your four-week-old forecast against actual cash position and note the variance. A consistent 15 percent variance signals that your assumptions about payment timing, churn, or customer acquisition costs are wrong and need recalibration. Most businesses discover their forecasts are too optimistic on collections and too conservative on expense timing-knowing your specific bias lets you adjust inputs rather than chase phantom accuracy.

Use a rolling 13-week forecasting window rather than calendar quarters. This forces continuous updates and prevents the trap of stale quarterly forecasts that no longer reflect reality. When week 14 arrives, drop the oldest week and add a new week 14, maintaining constant forward visibility. This rolling approach also aligns with how most banks and investors expect to see cash projections, making conversations about funding timelines or covenant compliance far more credible.

Extract Signal from Historical Data

Historical data becomes your baseline only after you separate signal from noise. Pull 18 to 24 months of actual cash inflows and outflows, then segment by revenue stream and customer cohort. A SaaS business with 5 percent churn learned from historical data might discover that churn actually runs 7 percent in months following price increases and 2 percent in months with major product releases. That insight lets you forecast more accurately around planned launches and pricing changes.

Seasonal patterns emerge only across multiple years, so if you have fewer than 12 months of data, flag seasonal assumptions as risks rather than facts. Retail businesses see this most acutely-Q4 revenue drives 40 to 50 percent of annual cash flow, yet a startup with only eight months of history cannot see this pattern yet. Apply conservative buffers to seasonal predictions until you have three years of data confirming the pattern.

Variable cost ratios shift as you scale, so recalculate payment processing fees, shipping costs, and contractor rates quarterly against actual revenue. A 2.9 percent Stripe fee that held true at $50,000 monthly revenue might shift to 2.2 percent at $500,000 monthly volume. These small changes compound across a 13-week forecast and materially affect your burn rate projections. Accounts receivable aging data from the past six months reveals your true collection pattern. If historical data shows customers consistently pay on day 50 despite net-30 terms, build that into every forecast going forward rather than optimistically assuming net-30. Collections acceleration initiatives like early payment discounts or automated reminders should show measurable improvement in aging reports within 60 days, validating whether the initiative actually works or just sounds good in theory.

Automate Data Feeds to Eliminate Manual Entry

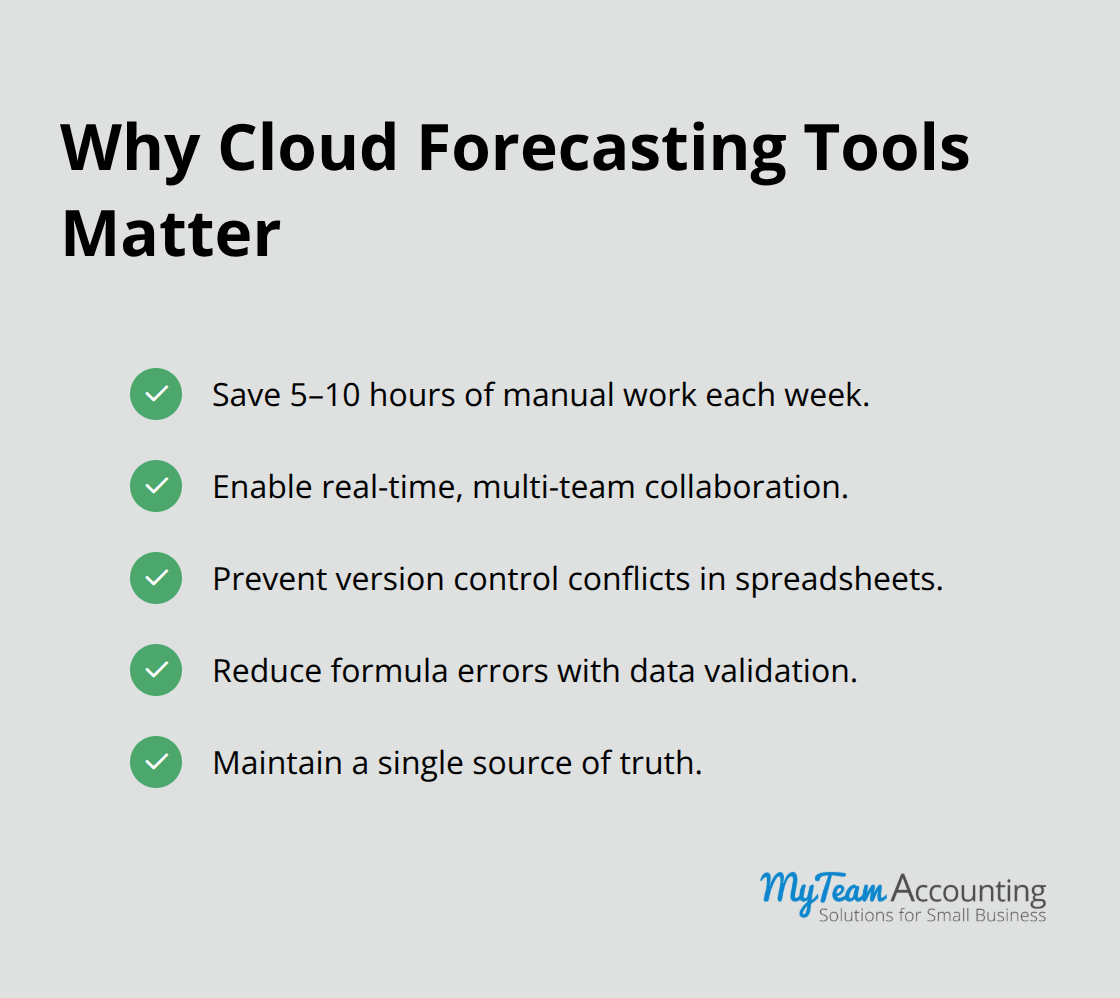

Technology integration eliminates the friction that kills forecast discipline. Connect your accounting software directly to your bank accounts so cash balances auto-refresh daily without manual entry. Link your invoicing system to track when payments actually post, not when invoices go out. If you use Stripe or another payment processor, pull transaction data automatically so revenue timing reflects actual customer payments, not accounting entries. This integration matters because manual forecasts require hours of data gathering that teams skip when busy, causing forecasts to decay into irrelevance. Automation makes weekly updates feasible for small teams.

Cloud-based forecasting tools integrate with QuickBooks and Xero, pulling transaction data and automatically calculating burn rates and runway. These tools cost $150 to $500 monthly but save five to ten hours of manual spreadsheet work per week, which justifies the expense immediately. More importantly, cloud tools enable real-time collaboration so your sales team can input pipeline changes and your operations team can adjust payroll forecasts without creating version control chaos. Spreadsheet-based forecasting fails at scale because multiple people edit the same file, creating conflicting versions and corrupted formulas. One person’s formula error cascades through the entire forecast and nobody catches it until cash runs short.

Set Alerts to Catch Drift Before It Becomes Dangerous

Set up automated alerts so you receive notifications when cash balance falls below a threshold you define, typically your minimum cash buffer of 10 to 15 percent of monthly outflows. An alert at $50,000 remaining cash gives you two weeks to act before a $10,000 daily burn exhausts reserves completely, versus discovering the problem when the account hits zero. Implement this alert today if you have not already, because it costs nothing and catches the single most dangerous cash scenario: gradual drift below safety thresholds that leadership does not notice until it is too late.

Final Thoughts

Dynamic cash flow forecasting transforms from a compliance exercise into a strategic advantage when you commit to weekly updates, real-time data integration, and honest scenario planning. The businesses that survive downturns and capitalize on growth opportunities see cash problems weeks in advance, not after payroll fails to clear. You now possess the framework: track revenue timing precisely, separate fixed from variable costs, update forecasts weekly, and extract signal from historical data.

Starting your forecasting system requires three immediate actions. First, pull 18 months of historical cash data and segment it by revenue stream and customer cohort to establish your baseline patterns. Second, connect your accounting software and bank feeds to eliminate manual data entry, then commit to a specific day each week for forecast review. Third, define your minimum cash buffer based on your burn rate and sales cycle length, then set automated alerts to notify you when cash approaches that threshold.

Professional advisory services accelerate this process significantly. A fractional CFO or financial consultant brings forecasting expertise, helps you build dynamic models that reflect your specific business model, and conducts weekly reviews that keep assumptions honest. They integrate real-time data across your systems, implement scenario planning that tests your strategy against market uncertainty, and communicate cash position to investors and lenders in language they understand. Whether you build this capability internally or partner with external expertise, you gain control over your financial future instead of remaining reactive to cash surprises.