Small Business Accounting Practices: Frameworks for Consistent Reporting

Accurate financial records are the backbone of every thriving small business. Without consistent reporting systems, you risk missed tax deadlines, compliance issues, and poor decision-making.

Small business accounting practices form the foundation for sustainable growth. This guide walks you through proven frameworks that ensure your finances stay organized, reliable, and audit-ready.

Building the Right Accounting Foundation

Structure Your Chart of Accounts for Decision-Making

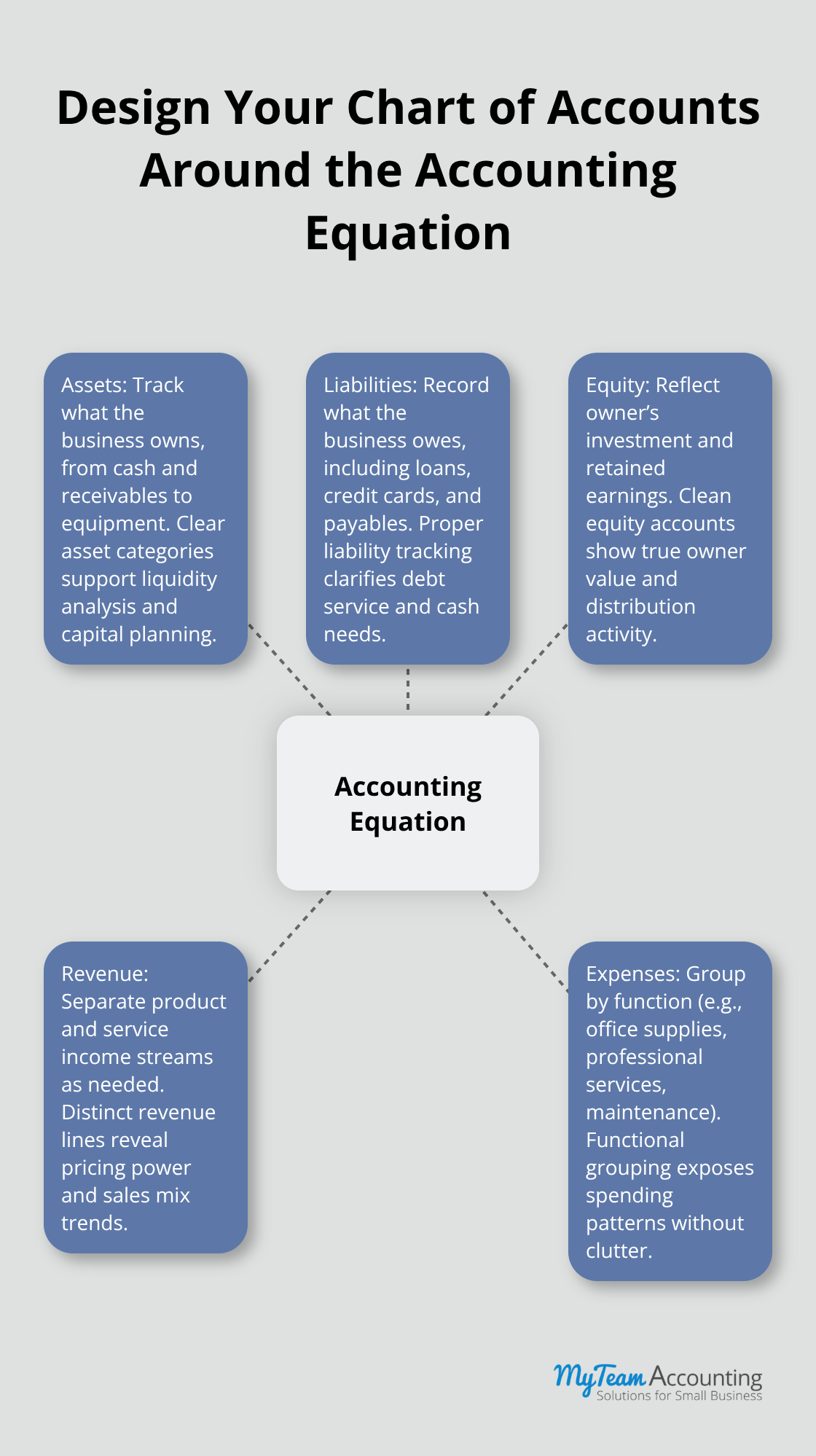

Your chart of accounts is not just a filing system; it shapes how you understand your business. Small business owners often either oversimplify their accounts into five or six catch-all categories or overcomplicate them with dozens of granular accounts that become impossible to manage. The sweet spot typically falls between fifteen and thirty accounts, organized by the accounting equation: assets, liabilities, equity, revenue, and expenses. Within expenses, segment accounts by function rather than by vendor. Instead of separate accounts for each supplier, create accounts for categories like office supplies, professional services, or equipment maintenance.

Your chart of accounts structure should align with how you actually run your business and the decisions you need to make monthly. If you sell both products and services, separate those revenue streams. If you operate multiple locations or channels, your account structure should reflect that reality. Start with a template tailored to your industry, then customize ruthlessly to match your operations. Your bookkeeper or accountant should build this structure with you upfront, not retrofit it after six months of chaotic data entry.

Maintain Discipline in Your General Ledger

Once your accounts are in place, your general ledger becomes the permanent record of every transaction, and discipline matters most here. The NFIB reports that roughly 65.3 percent of small businesses were profitable in 2022, and profitability visibility depends entirely on accurate ledger entries and timely reconciliation. Assign specific people to handle accounts receivable, accounts payable, cash management, and bank reconciliation-no exceptions. Monthly reconciliations between your bank statements and your ledger are non-negotiable; a mismatch of even a few dollars today becomes a nightmare during tax season or when preparing financial statements for lenders.

Many small business owners delay reconciliation because they assume it’s tedious busywork, but catching discrepancies early prevents fraud, catches duplicate entries, and ensures your monthly financial reports actually reflect reality. When preparing financial statements, follow the accrual basis of accounting, which records transactions when they occur rather than when cash changes hands. This approach gives you a true picture of profitability and aligns with how lenders and investors evaluate your business.

Present Three Essential Financial Statements

Your financial statements should include a balance sheet showing assets, liabilities, and equity; an income statement showing revenue and expenses; and a cash flow statement showing how cash actually moved through your business. These three statements tell different stories, and all three matter for decision-making. Standardize the format and timing of these reports so that month after month looks consistent, making trends immediately visible. If your revenue structure or expense categories shift, document the change and explain it in a footnote so comparisons remain meaningful.

With your chart of accounts structured, your ledger disciplined, and your financial statements standardized, you’ve established the technical foundation for reliable reporting. The next step involves operationalizing these frameworks through consistent monthly procedures that transform raw data into actionable insights.

How to Make Monthly Closes Automatic and Audit-Ready

Close Your Books in Five Days, Not Five Weeks

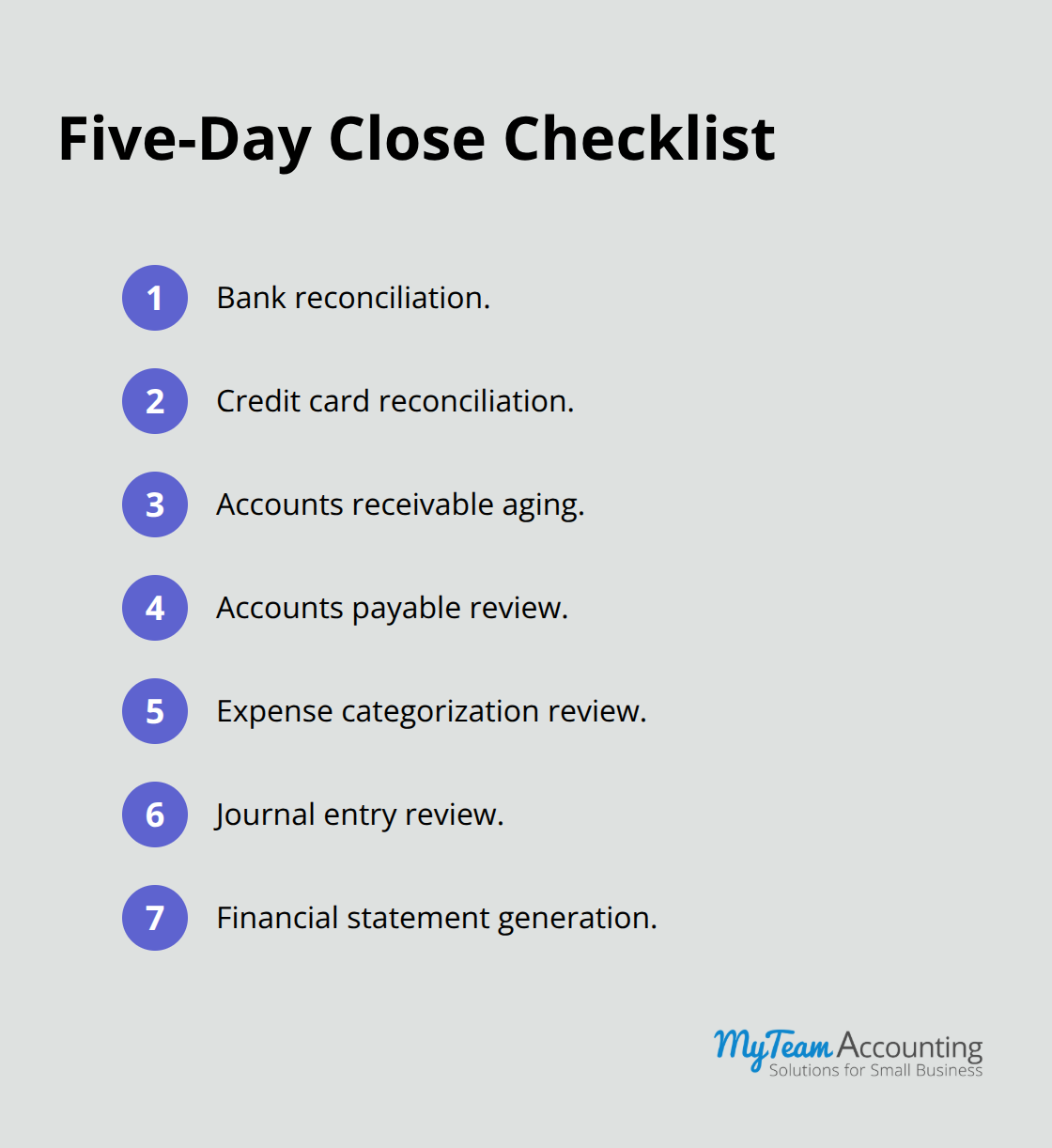

Close your books within five business days of month-end, not five weeks. Most small business owners treat month-end closing as an annual event rather than a disciplined monthly ritual, which means they miss cash flow trends, cannot answer basic profitability questions, and scramble during tax season. A five-day close is aggressive but achievable when you automate the right tasks and assign clear ownership. Start with your exact closing checklist: bank reconciliation, credit card reconciliation, accounts receivable aging, accounts payable review, expense categorization review, journal entry review, and financial statement generation. Assign one person to own each task and set a specific due date within your five-day window.

Automate Reconciliation to Save Hours Each Month

Reconciliation tools in QuickBooks Online and Xero flag unmatched transactions automatically, cutting reconciliation time from hours to minutes. Reconcile your bank weekly so that discrepancies surface before month-end arrives, not after. About 71 percent of small business owners use budgeting software, yet far fewer have systematized their actual close process. Your close procedure should remain identical every month, which means deviations from normal spending patterns, duplicate vendor payments, or unusual journal entries stand out immediately rather than hiding in year-end chaos. Create a standardized close checklist in a shared document or project management tool, assign task owners, set deadlines, and track completion. The discipline here is not about perfection; it is about catching problems before they compound.

Connect Your Data Feeds and Implement Auto-Categorization

Connect your bank feeds, credit card feeds, and vendor accounts directly to your accounting software so transactions appear automatically. This removes the manual data entry step entirely and ensures your records match your bank within days. Implement rules within your accounting software to auto-categorize recurring transactions like payroll, rent, or insurance premiums based on amount, vendor name, or description. A business that processes fifty transactions manually each month wastes hours that could be spent analyzing results instead.

Use Variance Analysis to Spot Trends Early

Variance analysis during financial close compares your actual cash inflows and outflows to forecasted amounts to quantify any differences, which forces you to ask why and adjust next month’s strategy. If your revenue was five percent below forecast, investigate whether that reflects a seasonal dip, a lost customer, or a timing issue. If expenses exceeded budget, categorize overages by department so you know whether the problem is payroll, supplies, or something else. This conversation happens during the close; it does not happen in tax season. Your standardized financial reports should display year-to-date results, prior-year comparisons, and budget variances on a single dashboard so trends jump out immediately. When you can see that customer acquisition cost is rising or that gross margin is shrinking, you can adjust pricing or operations before the problem becomes critical.

With your close process now running on schedule and your variance analysis revealing real-time performance gaps, you can shift focus to the mistakes that derail even disciplined accounting systems.

Where Your Accounting System Actually Breaks Down

The technical systems you build in month one crumble when personal and business finances blur together, when reconciliation becomes sporadic, and when expense categories shift based on whoever enters the data. These three failures are not theoretical risks; they are the reasons small business owners cannot answer basic questions about profitability and why tax season becomes a crisis.

Separate Personal and Business Finances Completely

Mixing personal and business finances destroys your audit trail and makes it impossible to know whether your business is actually profitable. Many owners justify this approach as temporary or promise to sort it out later, but later never comes. When you pay a personal expense from the business account or use the business account for a personal transfer, you create confusion that extends far beyond tax time. Your financial statements become unreliable because your actual business revenue and expenses are obscured by personal transactions.

If you ever need to refinance debt, apply for a business loan, or bring in investors, lenders will demand clarification on every mixed transaction, which costs you time and credibility. The solution is ruthless: open a separate business bank account and a separate business credit card, and never use them for personal expenses. If you need cash from the business, take a formal owner draw on a specific schedule rather than treating the account as your personal piggy bank. This discipline requires effort in month one but saves you dozens of hours and countless headaches later. Assign your bookkeeper or use accounting software rules to flag any transaction that looks personal so problems surface immediately rather than hiding for months.

Enable Audit Trails and Reconcile Monthly

Neglecting reconciliation and audit trails is perhaps the most dangerous mistake because it creates the illusion of control while exposing you to fraud, duplicate payments, and undetectable errors. A small business owner who reconciles quarterly instead of monthly might miss a vendor billing them twice for the same invoice or an employee submitting duplicate expense reports. When you close your books in five days as outlined earlier, reconciliation becomes a disciplined monthly habit rather than a year-end scramble.

The audit trail reporting in QuickBooks Online and Xero captures user activities and shows exactly who entered each transaction and when they entered it. If someone deletes a transaction or changes an amount, that change appears in the audit trail. Too many small business owners ignore this feature entirely, which means they have no way to investigate discrepancies when they occur. Enable audit trail reporting in your accounting software and review it monthly, especially for high-risk areas like cash transfers, journal entries, and payroll adjustments. If your bookkeeper or accountant cannot explain why a transaction appears in the audit trail, that is a red flag worth investigating immediately.

Enforce Consistent Expense Categorization Standards

Inconsistent expense categorization undermines your ability to manage costs and understand profitability by product, service, or customer segment. When one team member categorizes office supplies as office expenses and another categorizes them as general overhead, your spending data becomes meaningless. Over time, this inconsistency compounds until you cannot answer questions like how much you actually spend on marketing or whether a particular service line is profitable.

The solution requires a detailed chart of accounts that your entire team understands and a standardized categorization process that removes guesswork. Create a reference guide that shows exactly which types of expenses belong in each category, and require your bookkeeper to review all transactions weekly to catch categorization errors before they spread. If your accounting software offers auto-categorization rules based on vendor name or description, configure those rules aggressively so that recurring expenses categorize correctly without manual intervention. Train anyone who enters expenses on the correct categories and make it clear that vague categories like miscellaneous or other are not acceptable. When someone flags an expense as unclear, the bookkeeper should contact them immediately to clarify rather than guessing. This attention to detail in month one prevents the data quality problems that make month twelve impossible.

Final Thoughts

Small business accounting practices that prioritize consistency transform raw financial data into actionable intelligence for strategic decision-making. When you structure your chart of accounts thoughtfully, maintain a disciplined general ledger, and close your books monthly, you create a foundation where trends become visible and cash flow forecasting becomes accurate. A business that closes in five days rather than five weeks catches profitability problems early enough to adjust pricing or cut costs before margins erode.

The benefits of consistent reporting compound over time as your financial visibility improves. A business that separates personal and business finances knows exactly whether operations are actually profitable or whether owner draws mask underlying losses. A business that enforces consistent expense categorization can answer questions about which products, services, or customer segments drive real profit, and these insights replace guesswork with data-driven decisions.

Your next step depends on where you stand today. If you lack a formal chart of accounts, build one this week using a template tailored to your industry. If your close process takes weeks, pick one task to automate immediately, whether that means connecting your bank feed or implementing auto-categorization rules. Treat accounting as a non-negotiable operational discipline rather than a burden to outsource and forget, and let your financial data guide your business forward.