How Clean Books Lead to Better Tax Outcomes

Many small business owners dread tax season, but it doesn’t have to be stressful. The secret lies in maintaining clean books throughout the year, not scrambling to organize records when deadlines loom.

Accurate records are the foundation of tax-ready finances. When your bookkeeping basics are solid, tax preparation becomes straightforward, audit risk drops, and you uncover deductions you might otherwise miss.

This guide shows you exactly how to build and maintain the financial foundation your business needs.

Why Clean Books Matter Most at Tax Time

Documentation Protects Your Deductions

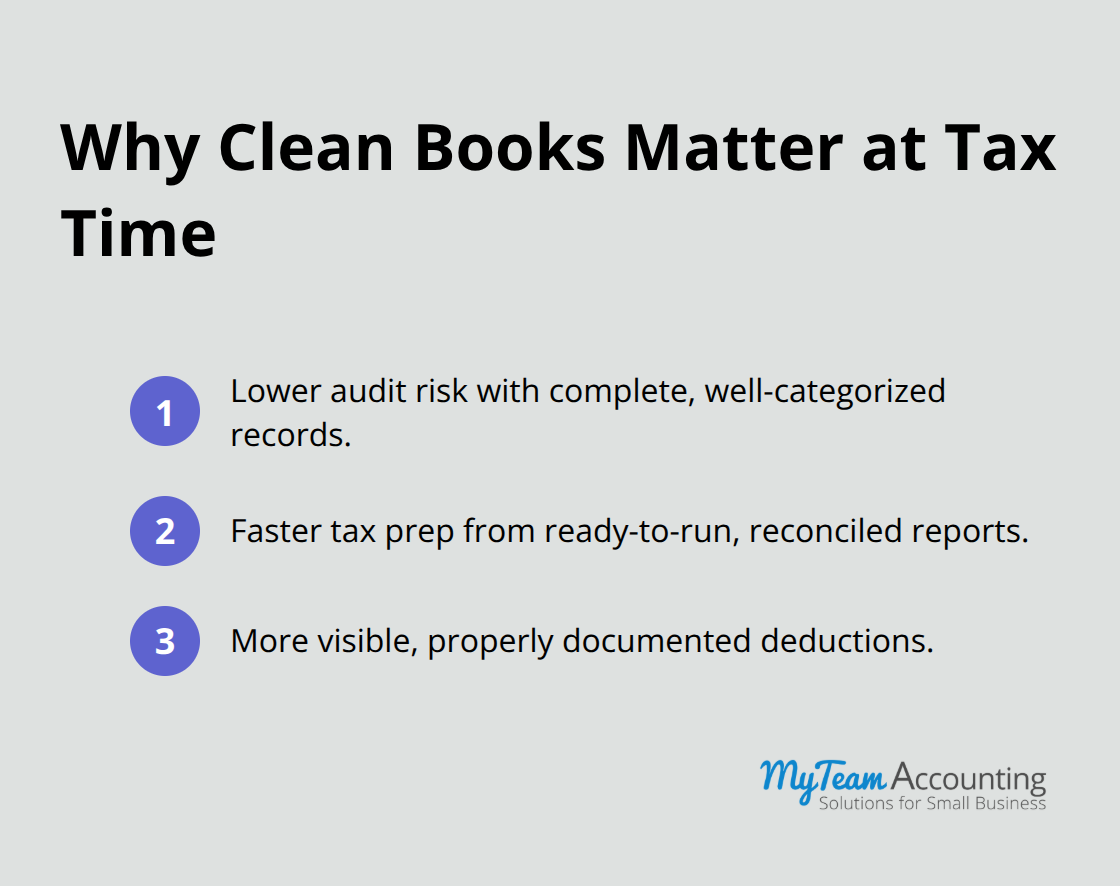

The IRS demands documentation, consistency, and proof that every number on your return reflects reality. Clean books eliminate guesswork and provide ironclad evidence that your tax position withstands scrutiny. When you organize records chronologically, categorize them correctly, and back them with receipts, audit risk drops dramatically. Most audits target businesses with gaps, inconsistencies, and vague expense categories-not those with meticulous records. A documented audit trail that matches invoices to bank statements to expense receipts transforms a potential crisis into a routine conversation. The real protection isn’t just compliance; it’s the confidence that comes from knowing every deduction can survive IRS review.

Without contemporaneous records showing what you spent and why it was business-related, the burden of proof shifts to you. Missing receipts or unclear categorization costs you money directly through IRS disallowance of deductions.

Tax Preparation Moves Faster and Costs Less

Tax preparation accelerates dramatically when your books stay current throughout the year. Instead of reconstructing transactions from six months ago, your accountant pulls reports that tell your business’s true story immediately. Organized financial data means your revenue reconciles to bank deposits, your expenses sit in proper categories, and your profit number proves accurate from day one. This speed translates directly into lower accounting fees because your tax preparer doesn’t bill hours hunting down missing transactions or reclassifying miscoded entries.

Visible Deductions Add Up to Real Tax Savings

Clean books reveal deductions that disappear into messy spreadsheets. Many small business owners claim less than half of eligible expenses simply because they never organized their records well enough to see what they spent. Utilities, contractor payments, software subscriptions, inventory costs, and equipment depreciation all hide in disorganized systems. When your bookkeeping system forces every transaction into a logical category, those deductions become visible and claimable. The difference between a small deduction and a properly documented one can total thousands of dollars in tax liability.

Understanding which mistakes destroy your deduction claims-and how to prevent them-separates tax filers who leave money on the table from those who capture every legitimate write-off.

The Mistakes That Drain Your Tax Savings

Misclassification Destroys High-Value Deductions

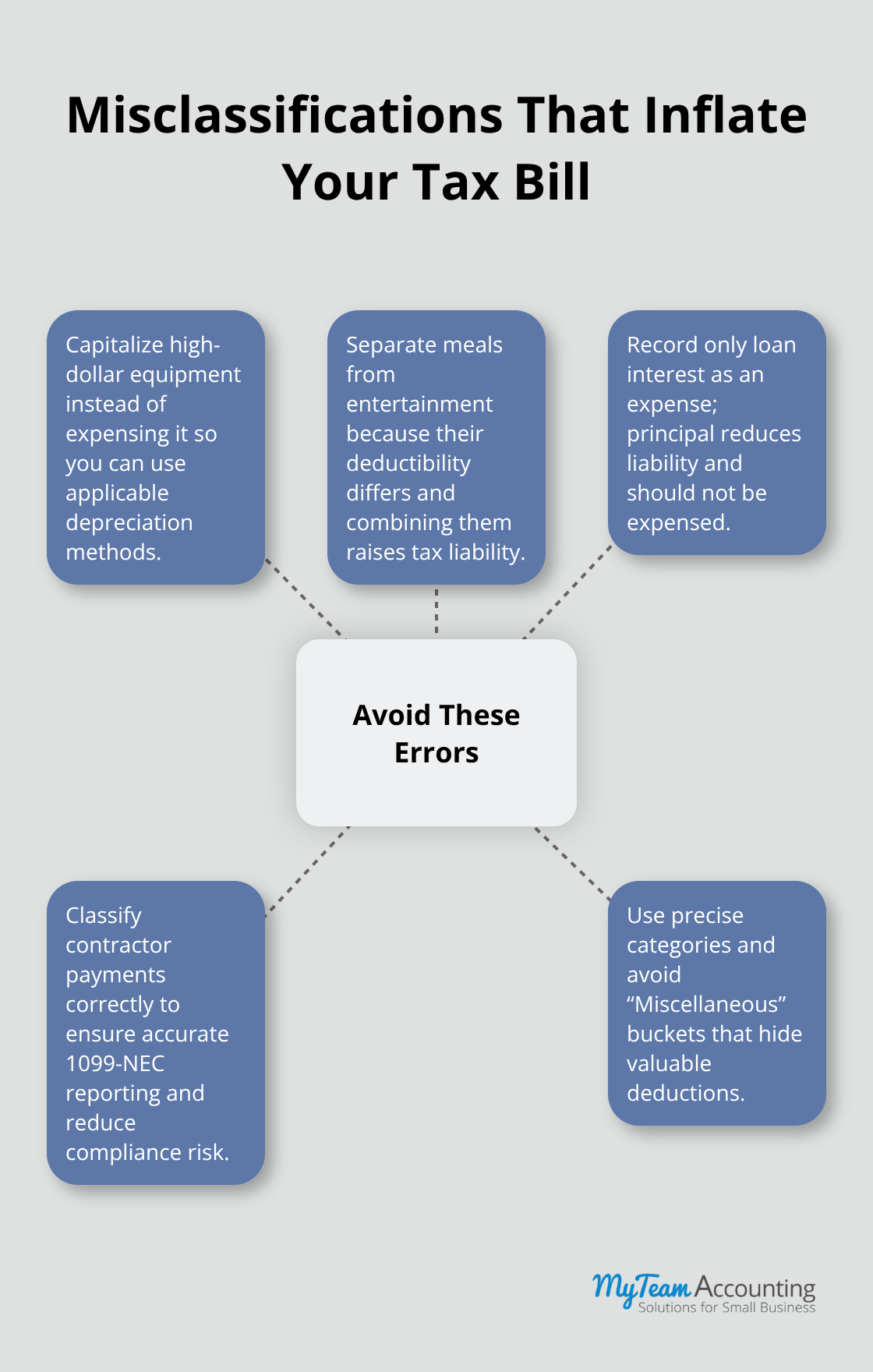

Misclassifying expenses destroys deductions before you ever file. When you expense a $3,000 laptop as office supplies instead of capitalizing it as a fixed asset, you miss Section 179 depreciation and Bonus Depreciation opportunities that could have reduced your taxable income significantly. Meals and entertainment get mixed into a single category, but the IRS allows only 50% of meal costs as deductible while entertainment is often 0% deductible-lumping them together inflates your tax liability. Loan principal payments frequently get coded as expenses when only the interest portion qualifies, overstating your deductions and distorting your actual cash flow. Contractor payments misclassified as wages trigger incorrect 1099-NEC reporting and create compliance risk. Vague categories like Miscellaneous or Other hide high-value deductions and signal disorganization to auditors.

Set a practical asset threshold, use precise category names that match your tax return, and treat every dollar like it matters because it does.

Missing Records Shift the Burden to You

Missing or incomplete records shift the burden of proof directly to you during an audit. The IRS assumes you owe tax on undocumented income, and without contemporaneous receipts showing what you spent and why it was business-related, deductions simply vanish. Small-dollar expenses compound silently-a $15 software subscription, a $40 client meal, a $100 office supply purchase each seem insignificant, but missing receipts for these items cumulatively erode thousands in tax savings annually. Not reconciling bank statements creates what accountants call ghost data: duplicate deposits, unrecorded bank fees, or fraudulent charges that distort your actual cash position and inflate reported income.

Capture receipts immediately through a mobile app that syncs with your accounting software, and reconcile monthly without fail. If a transaction lacks a business receipt, it should not appear in your books.

Commingled Finances Invite Audit Risk

Failing to separate personal and business finances makes it impossible to prove which expenses were truly business-related, pierces your corporate veil for liability purposes, and hands auditors an open invitation to disallow entire categories of deductions. A dedicated business checking account and business credit card establish clear boundaries between your personal spending and legitimate business costs. This separation strengthens your legal protection and provides the documentation auditors expect to see.

The fix requires discipline: use one business checking account and one business credit card, designate these accounts as your sole business payment method, and transfer funds to personal accounts through Owner’s Draw or Salary only. Clean separation isn’t optional-it’s the difference between audit-ready records and a tax nightmare. Understanding how to prevent these costly mistakes positions you to capture deductions that most business owners leave unclaimed, but the real power emerges when you implement systems that catch errors before they reach your tax return.

How to Build and Maintain Clean Books Year-Round

Design Your Chart of Accounts with Precision

Your chart of accounts is the skeleton of clean books, and most small business owners build it wrong. They start with software defaults, throw transactions at whatever category feels close, and wonder why their tax preparer questions half their deductions. Sit down before you process a single transaction and decide exactly where every dollar will live. This isn’t theoretical-it’s the difference between capturing deductions and losing them to vague categorization.

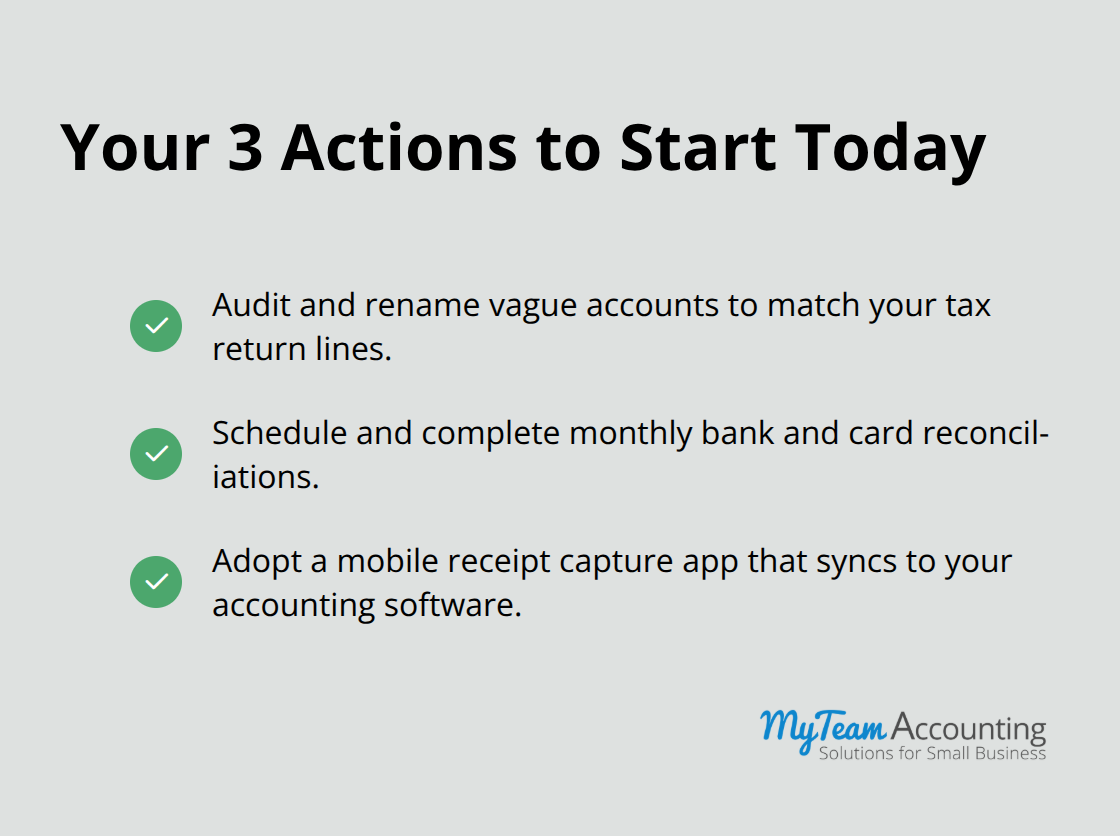

Create account names that match your tax return line items directly. If the IRS wants Office Supplies on Schedule C, call your account Office Supplies, not Supplies or Misc Materials. Separate meals from entertainment because they have different deduction rates. Split contractor payments by type-Professional Fees, Subcontractors, Consulting-so your 1099-NEC reporting aligns perfectly with how you actually hired people. Set a firm asset threshold, typically $2,500 and above, and force every purchase above that through a Fixed Assets account instead of expensing it immediately. This single decision prevents the catastrophic mistake of burying a $5,000 piece of equipment in office supplies and losing Section 179 depreciation entirely.

Name your accounts with precision and discipline. Vague categories like Other or Miscellaneous are audit red flags that signal disorganization and hide deductions. Every account should tell a story that your tax preparer can follow without asking questions. Software like QuickBooks automates transaction import and categorization, but automation only works if your chart of accounts is built correctly first.

Reconcile Monthly Without Exception

Monthly reconciliation is non-negotiable, and it must happen within days of month-end, not weeks later. Pull your bank and credit card statements the moment they arrive, open your accounting software, and match every transaction to your records. This catches duplicate deposits, unrecorded fees, fraudulent charges, and categorization errors before they compound into audit disasters. Most small business owners reconcile quarterly or annually, which means they discover problems months after the fact when fixing them is exponentially harder.

Set a calendar reminder for the third business day of each month and treat it like a client meeting-it cannot move. If your books don’t reconcile within an hour, something is wrong, and you need to find it immediately, not ignore it and hope it resolves itself.

Capture and Store Receipts Systematically

Capture receipts the moment you spend money. Mobile apps that sync directly to your accounting software eliminate the excuse of lost documentation. Take a photo of every receipt, every invoice, and every proof of payment. Store digital copies in a folder structure organized by month and category, not in a shoebox under your desk. The IRS expects contemporaneous records showing what you spent and why it was business-related. Without them, deductions vanish during audit. This discipline costs nothing except attention, but the alternative is thousands in disallowed deductions and penalties that destroy cash flow.

Final Thoughts

Clean books eliminate the chaos that costs small business owners thousands in missed deductions, audit risk, and wasted time. The investment in maintaining accurate records throughout the year pays dividends at tax time and beyond. When your bookkeeping basics remain solid, tax preparation becomes a straightforward process rather than a scramble to reconstruct months of transactions.

The real payoff extends far beyond tax season. Tax-ready books reveal which service lines are profitable, where cash actually flows, and whether your labor costs align with demand. This financial clarity becomes a leadership tool that speeds decisions, strengthens conversations with lenders and advisors, and builds accountability across your organization.