Employee Payroll Compliance: Keeping Payroll on Point

Payroll errors can be costly. Penalties, audits, and employee disputes arise when employee payroll compliance falls short. Understanding the rules and implementing the right systems protects your business and your team.

This guide walks you through common mistakes, essential requirements, and proven strategies to keep your payroll accurate and compliant.

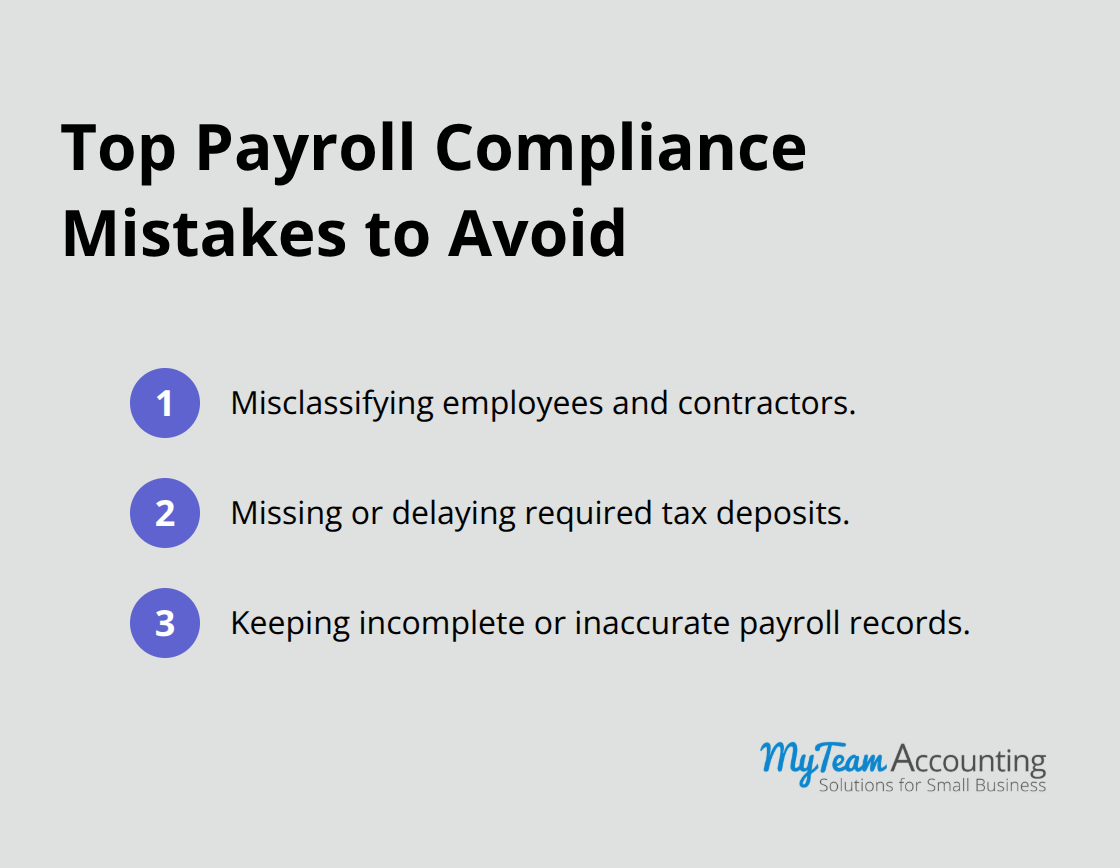

Common Payroll Compliance Mistakes

Where Payroll Classification Goes Wrong

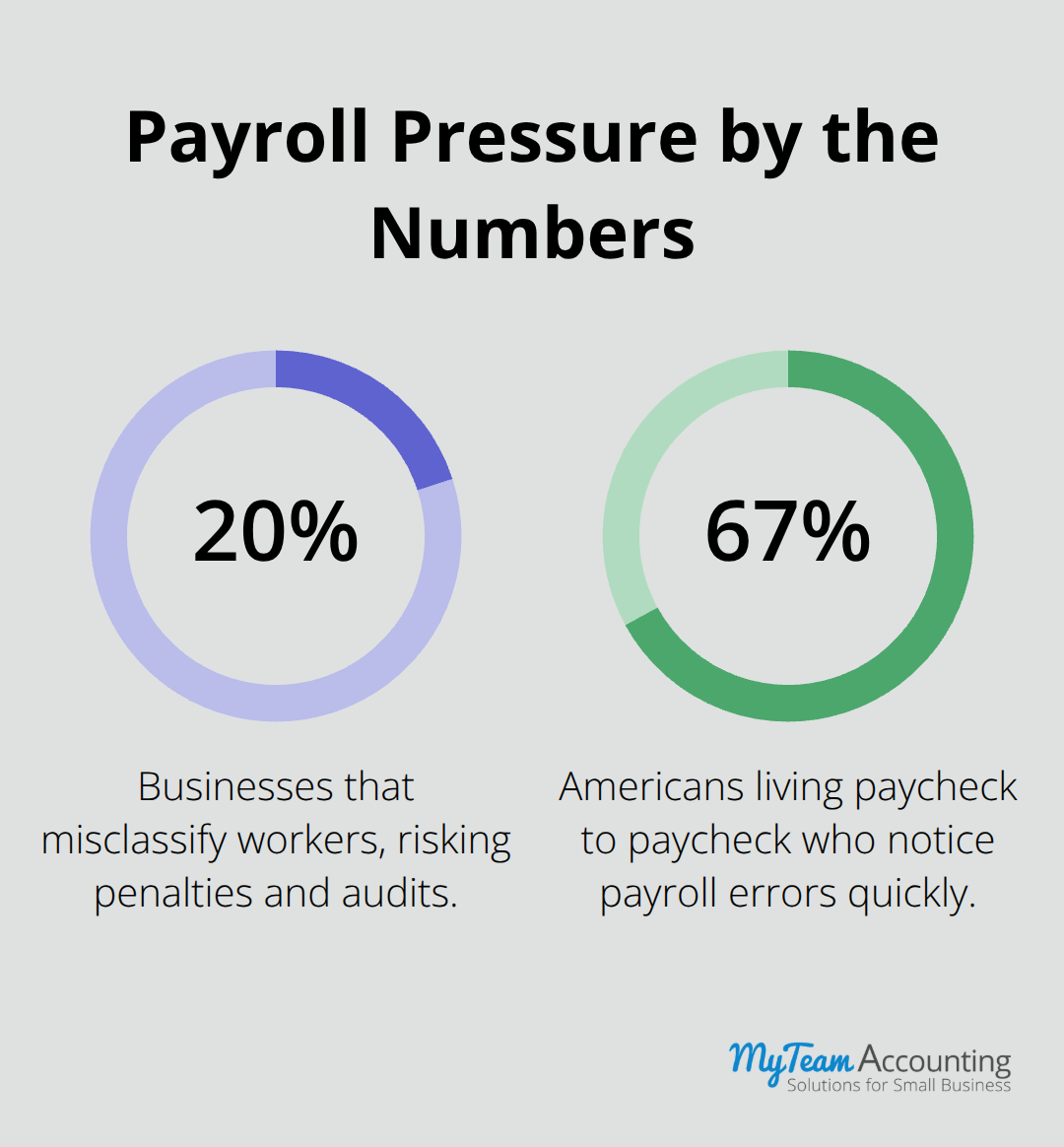

Misclassifying workers stands as the single most expensive payroll mistake businesses make. The IRS and Department of Labor use a worker classification three-part test to determine worker status: control over work, investment in tools and equipment, and profit or loss opportunity. Many businesses fail this test entirely. A worker who sets their own hours, uses company equipment, and cannot realize a profit or loss is an employee, not a contractor. Yet roughly 20 percent of businesses misclassify workers anyway, often to avoid payroll taxes and benefits obligations. The cost of this error proves severe. Penalties for misclassification run into thousands per worker, plus back taxes, interest, and potential lawsuits. The U.S. Department of Labor provides clear guidance on worker classification, and ignoring it exposes your business to audits that can span multiple years of payroll records.

The Tax Withholding and Deposit Trap

Failing to withhold federal income tax, Social Security, and Medicare creates a cascading compliance disaster. Federal tax deposits must hit specific dates tied to Form 941, and missing even one deadline triggers penalties. In 2024, businesses paid payroll tax withholding penalties 2024 $2.8 billion for incorrect or missed employee payments. Many owners assume they can catch up on deposits later or skip them during cash-flow crunches. This assumption proves critical and wrong. The IRS treats late deposits as willful violations, and penalties escalate quickly. Additionally, roughly one in three employees quit due to payroll problems, meaning tax withholding failures damage retention alongside your compliance standing. Automated payroll systems eliminate guesswork by calculating withholdings based on current W-4 data and scheduling deposits to match Form 941 requirements. Manual spreadsheets create blind spots where errors hide until an audit surfaces them.

Record Keeping That Actually Holds Up

The Fair Labor Standards Act requires employers to maintain pay records for three years, though some states demand longer retention. Many businesses keep incomplete records, missing hours worked, pay rates, or payroll dates. This creates vulnerability during wage-and-hour audits. If your records cannot prove you paid overtime correctly or applied minimum wage properly, the burden of proof shifts to you, and you lose. For non-exempt employees, time-tracking systems must capture actual hours, not estimates. Misclassifying someone as exempt when they should be non-exempt, then failing to track their hours, compounds the violation and multiplies back-pay exposure. A single wage-and-hour lawsuit can cost tens of thousands in legal fees alone, before settlements. Digital payroll platforms with integrated time tracking create an auditable trail that protects you in disputes and audits.

These three mistakes-misclassification, tax deposit failures, and poor record keeping-form the foundation of most payroll violations. Understanding what goes wrong sets the stage for learning what compliance actually requires.

What Compliance Actually Requires

Federal tax withholding and FICA tax rates sit at the core of payroll compliance, and the math is non-negotiable. Employees owe 7.65 percent in FICA taxes: 6.2 percent for Social Security on wages up to $184,500 in 2026, plus 1.45 percent for Medicare on all wages with no cap. You match that 7.65 percent as the employer. Federal income tax withholding varies based on each employee’s Form W-4 and current IRS Publication 15-T brackets, which range from 10 to 37 percent depending on income level. The IRS updates these brackets annually, and using outdated rates triggers underpayment penalties. Form 941 reporting ties directly to deposit schedules: semi-weekly filers must deposit within three business days of the pay period end, while monthly filers must submit by the 15th of the following month. A single missed deposit deadline costs you 2 to 10 percent of the unpaid amount in penalties, compounded by interest.

Navigate State and Local Tax Complexity

State and local tax obligations multiply your compliance burden significantly. Most states impose income tax, but five states-Florida, Nevada, South Dakota, Tennessee, and Wyoming-do not. However, if you employ workers in multiple states, each state’s wage-and-hour laws, unemployment tax rates, and income tax rules apply independently. Pennsylvania townships impose local payroll taxes on top of state obligations, Ohio enforces eight different municipal tax rates, and New Jersey demands separate state and local filings. A multi-state operation without proper tax configuration in your payroll system guarantees errors.

Each state’s unemployment insurance tax (SUTA) ranges from roughly 0.6 to 6 percent of the first $7,000 to $42,000 per employee, depending on the state and your experience rating. Federal unemployment tax (FUTA) adds another 0.6 to 6 percent on the first $7,000 per employee. Small businesses often underestimate this complexity and fail to configure their systems correctly.

Wage and Hour Rules Drive Your Overtime Obligations

The Fair Labor Standards Act minimum wage and overtime requirements mandate federal minimum wage at $7.25 per hour, but 29 states and Washington D.C. exceed this floor. California and Massachusetts lead at $16 per hour as of 2026, and these higher minimums apply regardless of federal rates. Overtime rules prove equally strict: non-exempt employees must receive at least one and one-half times their regular rate for all hours over 40 per week, and some states like California require daily overtime after 8 hours.

Misclassifying someone as exempt to avoid overtime costs thousands in back pay plus penalties. The DOL uses a duties test, not job titles, to determine exemption status. An employee earning $50,000 annually cannot be classified as exempt if they spend 30 percent of their time performing non-exempt duties. You must document the basis for every exemption classification and audit it annually. Wage-and-hour violations carry treble damages in many jurisdictions, meaning a $10,000 back-pay claim becomes $30,000 in court.

With 67 percent of Americans living paycheck to paycheck according to 2025 data, employees notice even small miscalculations and pursue claims aggressively. Automated payroll systems calculate overtime thresholds by state, track hours in real time, and flag misclassifications before pay runs process. Manual calculations invite rounding errors, missed overtime hours, and audit exposure that no business can afford.

How to Build Payroll Systems That Prevent Mistakes

Compliance stops being theoretical the moment a penalty notice arrives. The businesses that avoid costly errors do not rely on hope or manual processes-they engineer compliance into their payroll operations from day one.

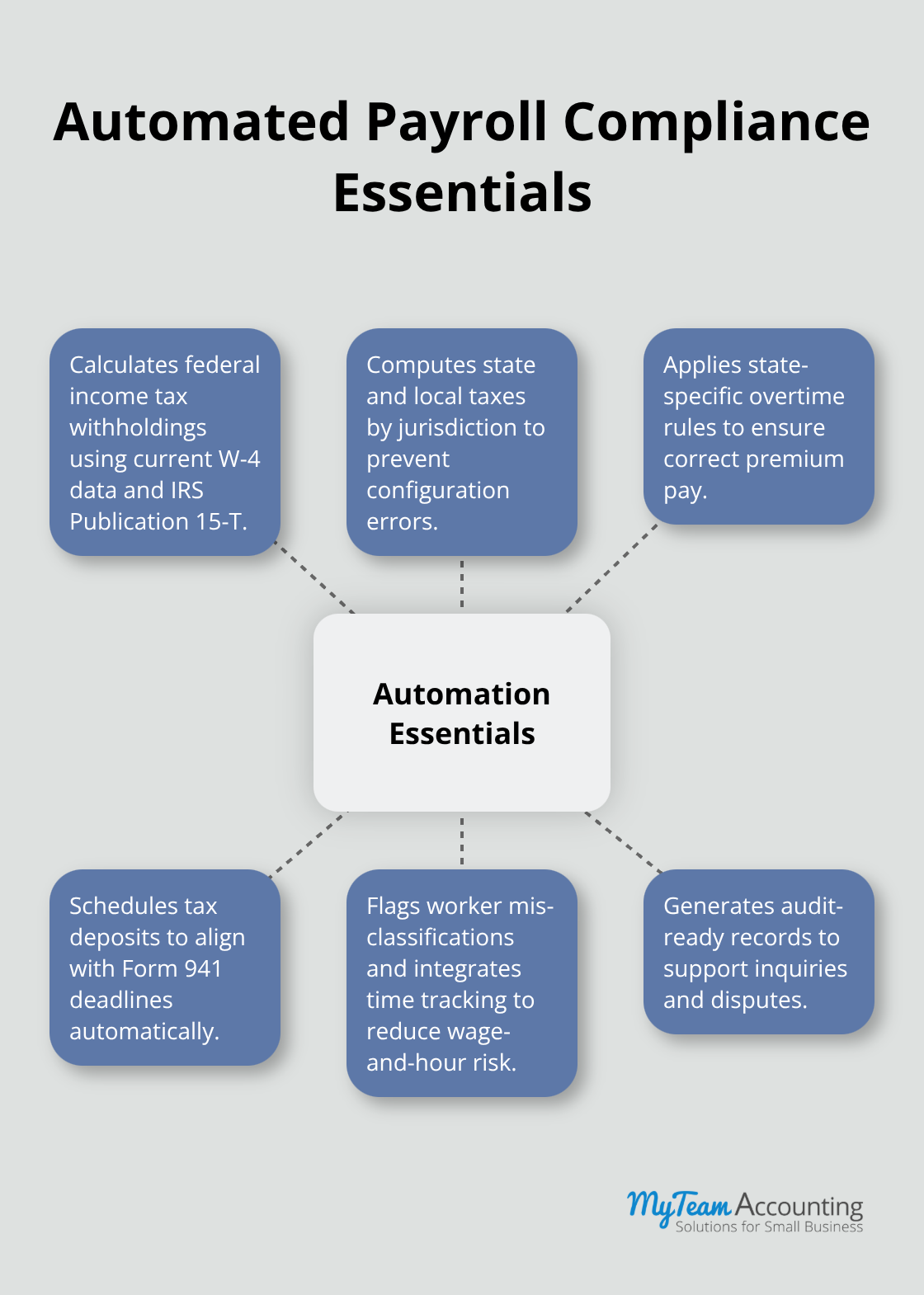

Automate Tax Calculations and Deposit Scheduling

Automation forms the backbone of compliance strategy because humans miscalculate taxes, miss deposit deadlines, and lose track of changing regulations. Payroll software eliminates these failure points entirely. When you configure your system correctly, it calculates federal withholdings based on current W-4 data and IRS Publication 15-T brackets, computes state and local taxes by jurisdiction, applies overtime rules specific to each state, and schedules tax deposits to align with Form 941 deadlines. The software flags misclassifications before pay runs process, integrates time-tracking data to prevent wage-and-hour violations, and generates audit-ready records automatically. This is not a luxury-it is the difference between staying compliant and facing audits that cost thousands in penalties and legal fees.

Small businesses often resist software investment, yet the average payroll error costs roughly 18 to 35 percent in savings when you factor in avoided penalties, reduced staff time, and eliminated manual errors. That calculation alone justifies the expense.

Conduct Monthly Payroll Audits

Automation alone cannot catch everything, which is why monthly payroll audits form your second line of defense. Pull your payroll reports each month and verify that tax deposits match Form 941 calculations, that overtime hours were paid correctly by state, that employee classifications remain accurate, and that deductions align with what employees authorized. Spot-check three to five pay stubs randomly to ensure gross-to-net calculations are correct and no unauthorized deductions appeared. When you conduct these reviews consistently, you surface problems in weeks instead of discovering them during an IRS audit years later.

Perform Quarterly Comprehensive Reviews

Beyond monthly checks, conduct a comprehensive payroll audit quarterly, reviewing your entire employee roster for misclassifications, auditing wage rates against job descriptions and responsibilities, and confirming that all state-specific requirements are met. The National Payroll Institute recommends this cadence specifically because payroll rules change constantly and small drift accumulates fast.

Monitor Regulatory Changes Actively

Stay current on regulatory updates through official IRS alerts and your state’s department of revenue guidance-do not rely on software vendors alone to notify you of changes. The IRS updates tax brackets annually, states change wage laws and unemployment rates regularly, and local jurisdictions add new requirements without warning. Assign one person accountability for monitoring these changes and updating your payroll system accordingly. This ownership prevents the scenario where a regulation changed six months ago but nobody noticed until an audit surfaces the violation.

Final Thoughts

Employee payroll compliance rests on three pillars: accurate classification, correct tax handling, and meticulous record keeping. Misclassify a single worker, miss one deposit deadline, or lose track of hours worked, and you expose yourself to penalties, audits, and legal disputes that drain resources and damage morale. The data confirms this reality-businesses that stay compliant avoid the $2.8 billion in annual penalties paid by companies that do not, and they retain employees who might otherwise quit over payroll errors.

The path forward requires automation, accountability, and attention to detail. Deploy payroll software configured for your specific jurisdictions, conduct monthly audits to catch drift early, and assign someone ownership of regulatory monitoring. These practices cost far less than recovering from violations, and they transform payroll from a source of stress into a reliable operational function.

Start today by running an internal audit of your current payroll processes and identifying your biggest vulnerability-whether misclassification, tax deposit gaps, or record-keeping gaps. If in-house expertise is limited, partner with a payroll provider or consultant who understands your industry and jurisdiction. The cost of getting payroll right is far lower than the cost of getting it wrong.