Payroll Compliance Checklist for Growing Small Businesses in 2026

As your small business grows, managing employee payroll becomes increasingly complex. Staying on top of payroll compliance isn’t optional-it’s essential to avoid costly penalties and legal issues.

This payroll checklist covers the critical rules and processes you need to implement right now. Whether you’re handling payroll processing manually or planning to upgrade your systems, this guide walks you through every requirement that matters for 2026.

Tax Deposits and Deadlines That Drive 2026 Compliance

Understanding Your Deposit Schedule and Lookback Period

The IRS modernization initiative demands near-real-time payroll reporting and stricter deposit schedules in 2026. Your deposit frequency depends on your lookback period, which the IRS calculates using tax liability from the prior four quarters. If your quarterly employment tax liability averages under $50,000, you deposit monthly. Once you cross $50,000, you shift to semiweekly deposits. An immediate trigger rule applies: if you accumulate $100,000 or more in taxes on any single day, you must deposit the full amount by the next business day. This shift can occur mid-quarter without warning, so tracking your running tax liability weekly becomes non-negotiable for compliance.

Federal Withholding, Social Security, and Medicare Taxes

Federal income tax withholding must account for 2026 tax tables and the redesigned Form W-4. Employees should complete the updated Form W-4 if their circumstances change, but if they don’t provide a new form, you continue using their last valid W-4 or apply default withholding rules. Social Security tax sits at 6.2% for both employer and employee on wages up to $184,500 in 2026, while Medicare tax is 1.45% with no wage cap. Additional Medicare Tax of 0.9% applies to employee wages exceeding $200,000, and you must withhold this from the employee’s pay. Supplemental wages like bonuses and commissions face a flat 22% federal income tax withholding rate unless total supplemental wages paid to that employee in the year exceed $1 million, which triggers 37% withholding instead.

State and Local Tax Complexity Across Jurisdictions

State and local tax requirements vary dramatically depending on your location and where employees work. If you employ remote workers across multiple states, you’re responsible for withholding based on the employee’s work state, not your office location. California requires withholding on all income earned within the state; Colorado has a flat 4.4% income tax; Texas has no income tax at all. Each state also maintains its own unemployment insurance system (SUTA), and rates fluctuate annually based on your experience rating and industry. Arizona mandates at least twice-monthly pay, while other states allow monthly payments. Missing a state deadline costs more than federal penalties because states often compound interest on unpaid taxes. Multi-state employers face significant compliance burden. Consolidating your payroll system across jurisdictions dramatically reduces fragmentation and mapping errors.

Quarterly and Year-End Filing Requirements

Quarterly Form 941 filings reconcile federal income tax withholding, Social Security, and Medicare taxes. Annual Form 940 covers Federal Unemployment Tax Act obligations at 6.0% on the first $7,000 of wages per employee, though you can credit up to 5.4% for state unemployment taxes you’ve already paid, reducing your net FUTA liability. Missing these filings or filing inaccurately triggers escalating penalties that compound quickly. Year-end W-2 forms must be issued and filed by January 31, and penalties for late or incorrect W-2s range from $110 to $260 per form depending on when you file and company size. The IRS now uses automated cross-checking between employer filings and employee tax returns, so even small discrepancies between your quarterly 941 and your year-end W-2 totals trigger audits. Set up electronic filing through the Social Security Administration’s Business Services Online portal before year-end to avoid last-minute delays.

Building Your Payroll Calendar for 2026

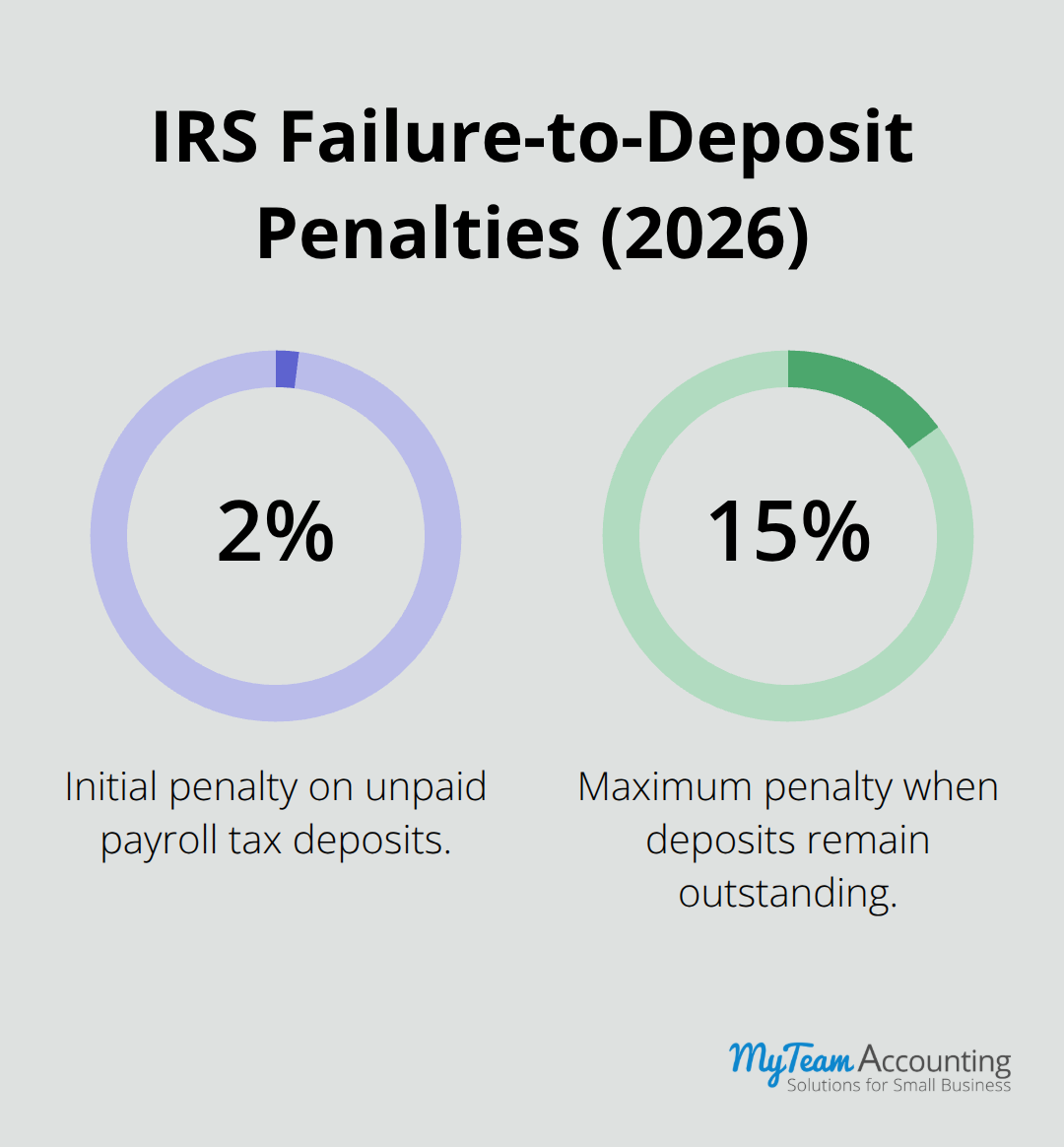

Your payroll calendar should map every deposit date, quarterly filing deadline, and year-end requirement month by month so deadlines never slip. Failure to deposit payroll taxes on time triggers penalties that escalate quickly: the IRS assesses failure-to-deposit penalties starting at 2% of the unpaid amount, climbing to 15% if deposits remain outstanding. More critically, the trust fund recovery penalty applies to responsible officers personally if employment taxes are withheld but not remitted, making this a personal liability issue, not just a business one.

Payroll Documentation That Protects Your Compliance

Complete, accessible records from day one separate compliant businesses from those facing audit penalties and wage disputes. The IRS and Department of Labor expect you to maintain employment eligibility verification, timekeeping logs, wage calculations, tax withholdings, and deduction authorizations for every employee throughout their tenure and for several years after separation.

I-9 Verification and Employment Eligibility Records

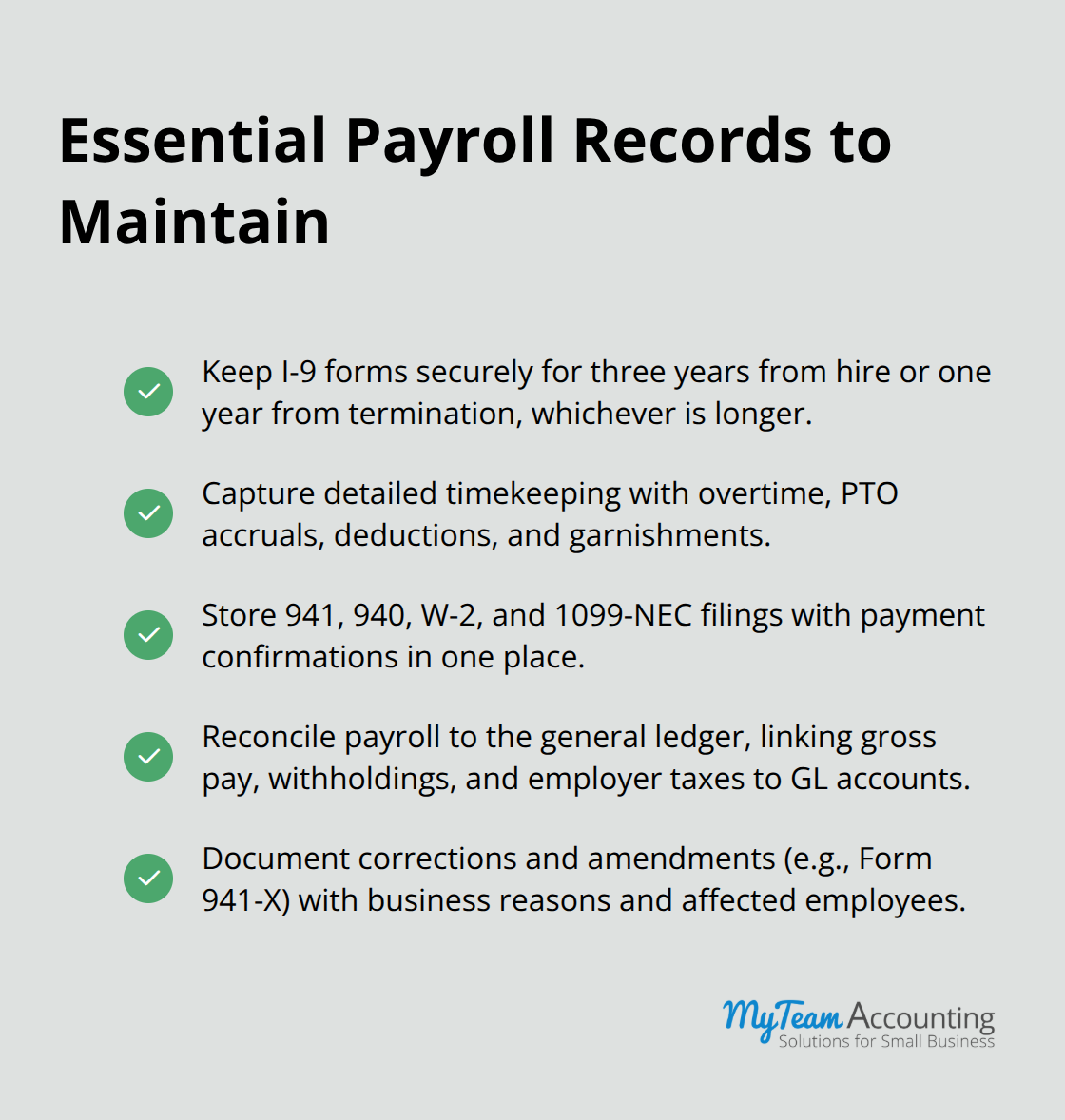

Form I-9 verification must occur within three days of hire and storage must remain secure for at least three years from hire date or one year from termination, whichever is longer. Your I-9 file should include the original completed form, copies of identity documents, and records of any E-Verify verification attempts if you use that system. Many small business owners skip this step or store I-9s haphazardly, creating immediate exposure to Department of Homeland Security penalties ranging from $230 to $2,300 per employee for document violations. Proper I-9 management protects both your business and your employees’ work authorization status.

Wage and Hour Records That Withstand Audits

Your wage and hour records must capture every hour worked, overtime calculations, paid time off accruals, deductions taken, and garnishments applied. The Fair Labor Standards Act requires you to maintain these records with enough detail to reconstruct gross pay, withholdings, and net pay for any pay period an employee disputes. If your timekeeping relies on paper timesheets or mental notes from managers, calculation errors compound across payroll cycles and create audit risk. Digital time tracking systems with audit trails eliminate this exposure entirely because they timestamp entries, flag overtime automatically, and prevent retroactive changes without documentation.

Tax Filing Records and GL Reconciliation

Your tax filing records must connect quarterly Form 941 filings to year-end W-2s with zero discrepancies. The IRS now cross-checks these filings electronically, so if your quarterly Social Security wage total differs from your W-2 Social Security wage total by even $100, automated systems flag the inconsistency for audit. Store copies of every 941, 940, W-2, 1099-NEC, and corresponding payment confirmations in one centralized location with clear date labeling. Your payroll-to-general ledger reconciliation should show how payroll expenses flowed into your accounting records, connecting gross pay, taxes withheld, and employer taxes paid to specific GL accounts.

Corrections, Amendments, and Change Documentation

Maintain documentation of any corrections or amendments you filed, including Form 941-X submissions and the business reason for the change. Many growing businesses make payroll adjustments mid-year for misclassifications or missed overtime but fail to document why the change occurred or which employees were affected, leaving auditors unable to verify the adjustment’s legitimacy. Set a quarterly reminder to reconcile your payroll records against your GL, verify that W-4 forms remain current for all employees, and confirm that any policy changes to pay frequency, deduction rates, or garnishment handling were communicated to affected staff in writing. This proactive documentation discipline costs minimal time upfront but eliminates the scramble when auditors request records and prevents costly disputes over wage calculations or tax withholdings. With your documentation systems in place, the next critical step involves identifying and avoiding the payroll mistakes that trigger the largest penalties and audit exposure.

Common Payroll Mistakes to Avoid

Misclassification of Employees vs. Contractors

Employee versus contractor classification determines whether you withhold payroll taxes, pay employer taxes, provide benefits, and comply with wage and hour laws. The Department of Labor reports that misclassification ranks among the most common violations in small business payroll. The Fair Labor Standards Act uses a multi-factor test that examines control, investment, permanence, and economic dependence-not simply what you call the worker or what they prefer. A contractor who works exclusively for your business, uses your equipment, follows your schedule, and cannot work for competitors simultaneously will be reclassified as an employee during an audit, triggering immediate liability for unpaid payroll taxes, Social Security, Medicare, unemployment insurance, and wage and hour violations spanning multiple years. State auditors prove particularly aggressive on this issue because misclassified workers drain state unemployment funds.

Department of Labor misclassification violation penalties can reach $25,000 per violation in some states, making reclassification urgent if you employ field technicians, drivers, or support staff classified as contractors to avoid payroll processing. The cost to reclassify and process back payroll falls far short of the penalty exposure. Conduct an internal review of every contractor relationship and document your classification rationale using Department of Labor guidance. If a worker meets any of these criteria-works full-time, uses company equipment, cannot refuse assignments, or cannot hire replacements-they belong on payroll as an employee, not on a 1099.

Missed Deadlines and Penalty Prevention

Missed tax deadlines and manual processing errors compound into cascading penalties that grow exponentially. The IRS assesses failure-to-deposit penalties starting at 2% of unpaid taxes, escalating to 10% if the failure spans 10 or more days, and reaching 15% for deposits outstanding more than 25 days. A single missed semiweekly deposit of $8,000 in payroll taxes triggers a minimum $160 penalty, but if that deposit remains unpaid for three weeks, the penalty jumps to $1,200 on top of accrued interest. Year-end W-2 penalties add another layer: filing even one day late costs $110 per form for businesses with 250 or more forms, and the IRS enforces these penalties rigidly with minimal reasonable-cause exceptions.

Manual payroll processing introduces calculation errors that cascade through multiple pay periods before discovery. One missed overtime calculation on an employee’s biweekly check compounds into 26 missed calculations annually, creating wage disputes and Department of Labor exposure. Growing businesses that rely on spreadsheets or manual calculations face audit risk because payroll data cannot be reliably reconstructed, tax withholdings appear arbitrary, and corrections lack audit trails.

Inadequate Systems and Manual Processing Errors

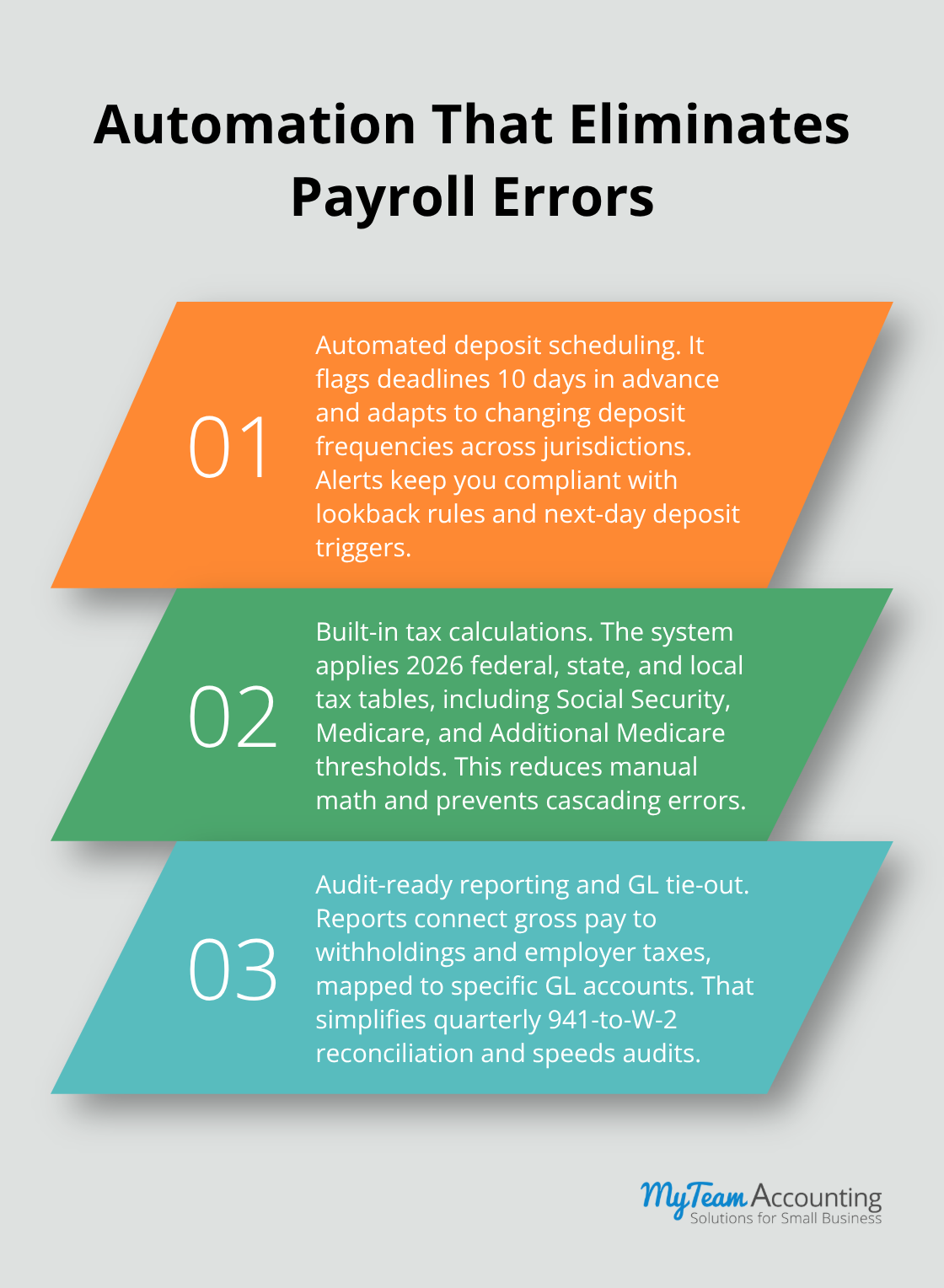

The solution to prevent these errors is straightforward: implement a payroll system with automated deposit scheduling that flags deadlines 10 days in advance, automates tax calculations using current 2026 tax tables, and generates audit-ready reports that connect gross pay to tax withholdings to GL accounts. A system eliminates the mental burden of tracking deposit schedules across multiple jurisdictions and removes the calculation errors that trigger wage disputes. The cost of payroll software or outsourced payroll processing proves negligible compared to the penalty exposure and the owner time spent managing manual processes.

Final Thoughts

Your payroll compliance checklist for 2026 centers on three non-negotiable priorities: accurate tax deposits tied to your lookback period, complete documentation that survives audit scrutiny, and systems that eliminate manual processing errors. These three areas account for the vast majority of penalties small businesses face, and you must address them now to prevent costly corrections later. The IRS modernization initiative and expanded real-time reporting demands mean that 2026 will expose payroll gaps faster than ever before, particularly for businesses that operate across multiple states where each jurisdiction maintains separate withholding rules, unemployment rates, and filing deadlines.

Outsourcing your payroll processing transfers both the operational burden and the compliance responsibility to professionals who track regulatory changes continuously. A payroll provider handles deposit scheduling, tax calculations, quarterly filings, and year-end reporting using current tax tables and jurisdiction-specific rules, while also providing access to compliance guidance when your business structure changes, you hire remote workers, or you expand into new states. The cost of outsourced payroll processing typically ranges from $25 to $100 per employee monthly, a fraction of the penalty exposure and owner time spent managing spreadsheets.

Start implementing your payroll checklist immediately by conducting a comprehensive audit of your current employee classifications, timekeeping records, and tax filing history. Verify that your I-9 documentation is complete and properly stored, your wage calculations align with state overtime rules, and your quarterly filings reconcile with year-end W-2 totals. Schedule a payroll compliance review with a qualified provider to identify specific risks in your operation and create a roadmap for 2026.