How to Build a Cash Flow Forecast That Actually Helps You Make Decisions

SILENT CLASSIFICATION: TASK_CLASS=ACTIVE (blog post chapter task)

Running a small business means juggling countless decisions daily. Without visibility into your cash position, you’re essentially flying blind, risking missed opportunities and unexpected financial strain.

Cash flow forecasting transforms raw financial data into a strategic tool. By projecting your business cash flow across weeks and months, you gain the clarity needed to make confident decisions about hiring, investments, and growth initiatives.

This guide walks you through building a practical forecast that actually drives results, not just sits in a spreadsheet.

Why Cash Flow Forecasting Actually Matters

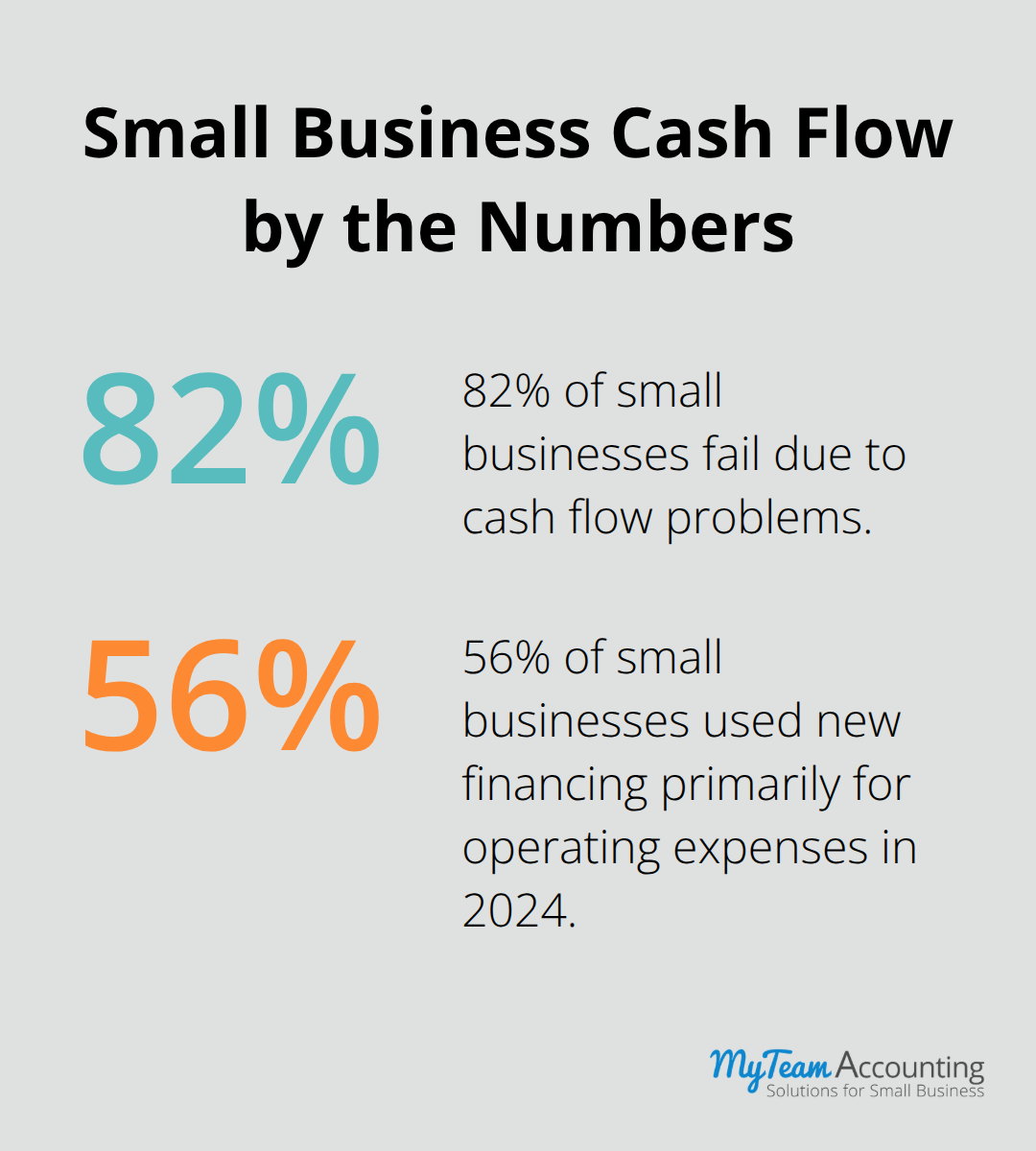

Most small business owners operate on financial autopilot, checking their bank balance occasionally and hoping it stays positive. This approach fails because your bank balance reflects the past, not the future. Cash flow forecasting flips this dynamic and shows you exactly when cash shortfalls will occur, often weeks before they happen. Consider this: 82% of small businesses fail due to cash flow problems. A business can be profitable on paper yet collapse because invoices arrive after bills are due. Forecasting exposes these timing mismatches before they become crises. When you project your cash position across the next 13 weeks, you spot the moment when accounts payable spike or when seasonal revenue dips. This advance warning lets you negotiate extended payment terms with suppliers, arrange a line of credit, or adjust spending-actions that prevent the panic of an unexpected shortfall.

The Strategic Advantage of Knowing What’s Coming

Forecasting transforms cash flow from a reactive metric into a decision-making tool. Rather than asking yourself whether you can afford to hire that new team member, you consult your forecast and see exactly when cash will be available. This clarity eliminates guesswork from major decisions. A solid forecast changes this entirely-you invest in equipment during cash-rich periods and hold back during lean months. You time hiring to match revenue growth rather than hoping revenue will follow hiring. You pursue opportunities like seasonal inventory expansion or market expansion because your forecast proves you can sustain the investment. Businesses that forecast cash flow make faster, more confident decisions about pricing adjustments, supplier negotiations, and expansion timing. They also maintain stronger relationships with lenders and investors because they demonstrate fiscal discipline through reliable projections.

Prevention Over Crisis Management

The cost of poor forecasting extends beyond missed opportunities. Without visibility into future cash needs, businesses overborrow, creating unnecessary debt obligations. They make poor investment decisions because they lack context about cash availability. They damage credibility with stakeholders when promised payments are delayed. A cash flow forecasting report prevents all of this and shows you exactly what you can and cannot afford. It also builds organizational accountability. When your team understands that cash matters and sees the forecast regularly, spending becomes more disciplined. Expenses get questioned. Collections improve because everyone recognizes that late payments create real problems. This shift from reactive crisis management to proactive planning delivers the greatest value-not in perfect predictions, but in giving you time to act.

What Separates Forecasters from the Rest

The difference between businesses that thrive and those that struggle often comes down to one factor: visibility. Companies that forecast cash flow know their financial position weeks in advance. They understand their seasonal patterns, their payment cycles, and their cash constraints. This knowledge allows them to make decisions with confidence rather than hope. The forecast becomes a living document that you update regularly, adjust for external shocks, and use to inform practical steps like pricing changes, credit term adjustments, or supplier payment renegotiations. Without it, you react to problems after they arrive. With it, you prevent problems from arriving in the first place.

The next step is understanding how to actually build this forecast. The process is simpler than most business owners expect, and it starts with the data you already have.

Building Your Forecast from Real Numbers

Gather Your Historical Data and Spot Patterns

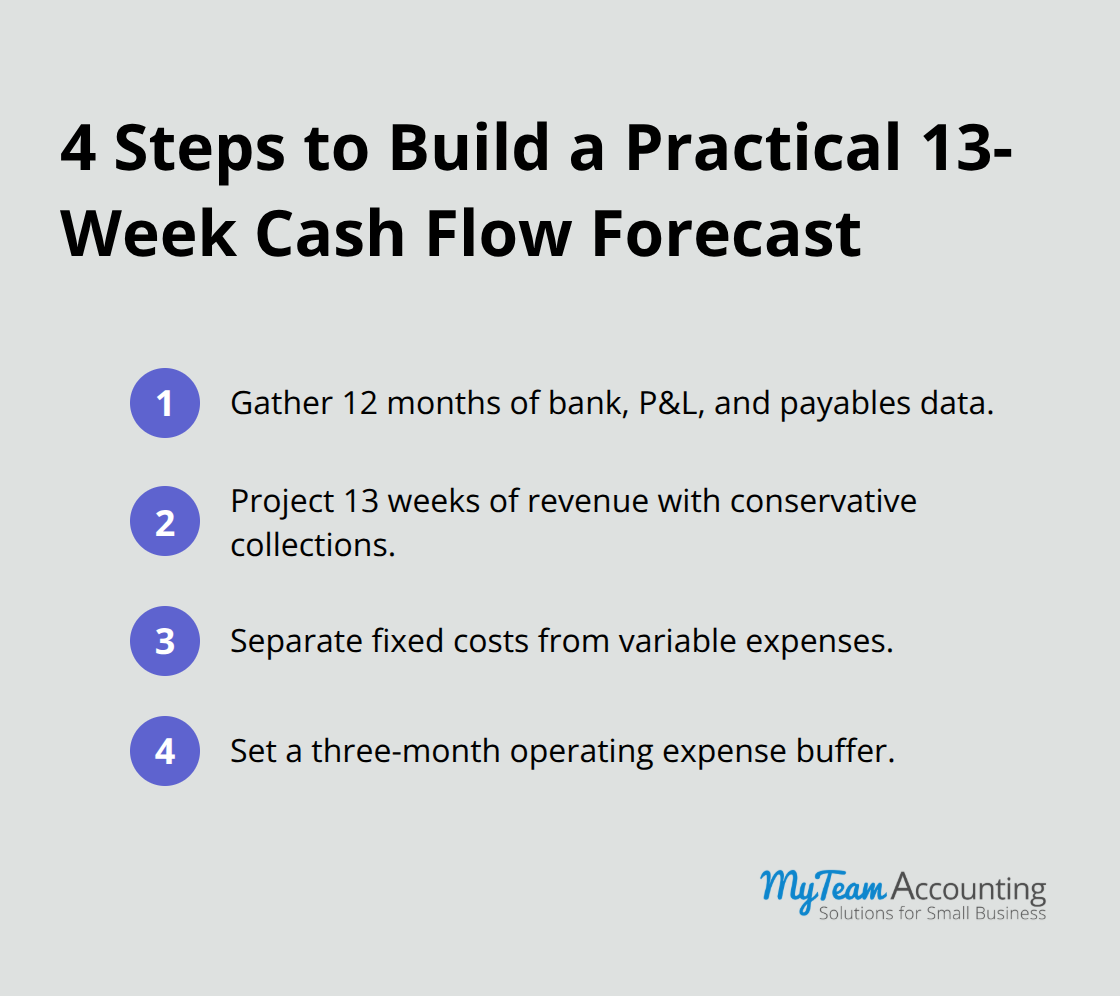

Start with your last 12 months of bank statements, profit and loss statements, and accounts payable records. This isn’t optional-it’s the foundation. Open a simple spreadsheet and list every deposit and expense by category: revenue, payroll, rent, supplies, taxes, loan payments, and anything else that moves cash. Look for patterns immediately. Did revenue spike in certain months? Did expenses cluster around specific dates? Historical cash flow patterns in seasonal businesses can create significant cash flow challenges for companies trying to make payroll or pay vendors during times of slower revenue. A service business with quarterly tax payments faces predictable cash drains. These patterns are gold. They reveal when your cash position will tighten and when you’ll have breathing room. If you’ve been in business less than a year, use industry benchmarks from trade associations relevant to your sector to estimate seasonal swings. The Federal Reserve noted that 56% of small businesses used new financing primarily for operating expenses in 2024, often because they failed to anticipate seasonal dips. Don’t repeat this mistake.

Project Revenue with Conservative Assumptions

Once patterns emerge, project your revenue conservatively for the next 13 weeks. Not optimistically-conservatively. Assume collection takes longer than invoices suggest. If you invoice on net-30 terms, assume some clients pay on day 45. If you sell products, account for returns and chargebacks. This is where most forecasts fail: business owners project what they hope will happen, not what actually happens. A 13-week rolling forecast works best because it maintains a quarterly view while staying current. Update it weekly as actual cash arrives, then extend it another week forward. This keeps your forecast always 13 weeks ahead without the maintenance burden of annual projections.

Account for Fixed and Variable Expenses Separately

Project expenses with brutal honesty. Fixed costs like rent and salaries stay constant, but variable costs like materials and shipping fluctuate with revenue. The mistake most owners make is grouping everything together instead of separating what changes from what doesn’t. This matters because fixed costs don’t disappear when revenue dips, which is when cash stress hits hardest. Calculate your opening balance for week one, add projected inflows, subtract all outflows, and you have your closing balance. That closing balance becomes next week’s opening balance.

Build in a Safety Buffer

Include a buffer-most experts recommend holding three months of operating expenses in reserve. If your monthly burn is $15,000, maintain a $45,000 minimum. This prevents panic decisions when unexpected expenses arrive or a major client delays payment. Tools like QuickBooks or Xero can automate much of this work by pulling actual bank and expense data, but the logic remains the same: know where cash comes from, know where it goes, and know when timing mismatches create shortfalls. This forecast becomes your decision-making lens for the next chapter, where you’ll learn how to actually use it to spot opportunities and plan your next moves.

How Your Forecast Reveals What Actually Matters

Your forecast now exists. The next step separates decisive business owners from those who build forecasts and ignore them. The real power emerges when you treat your projection as a living tool and use it to answer the specific questions that drive your business forward. Your forecast reveals three critical insights: when cash pressure arrives and why, where you leave money on the table, and exactly when you can afford to invest in growth without jeopardizing stability.

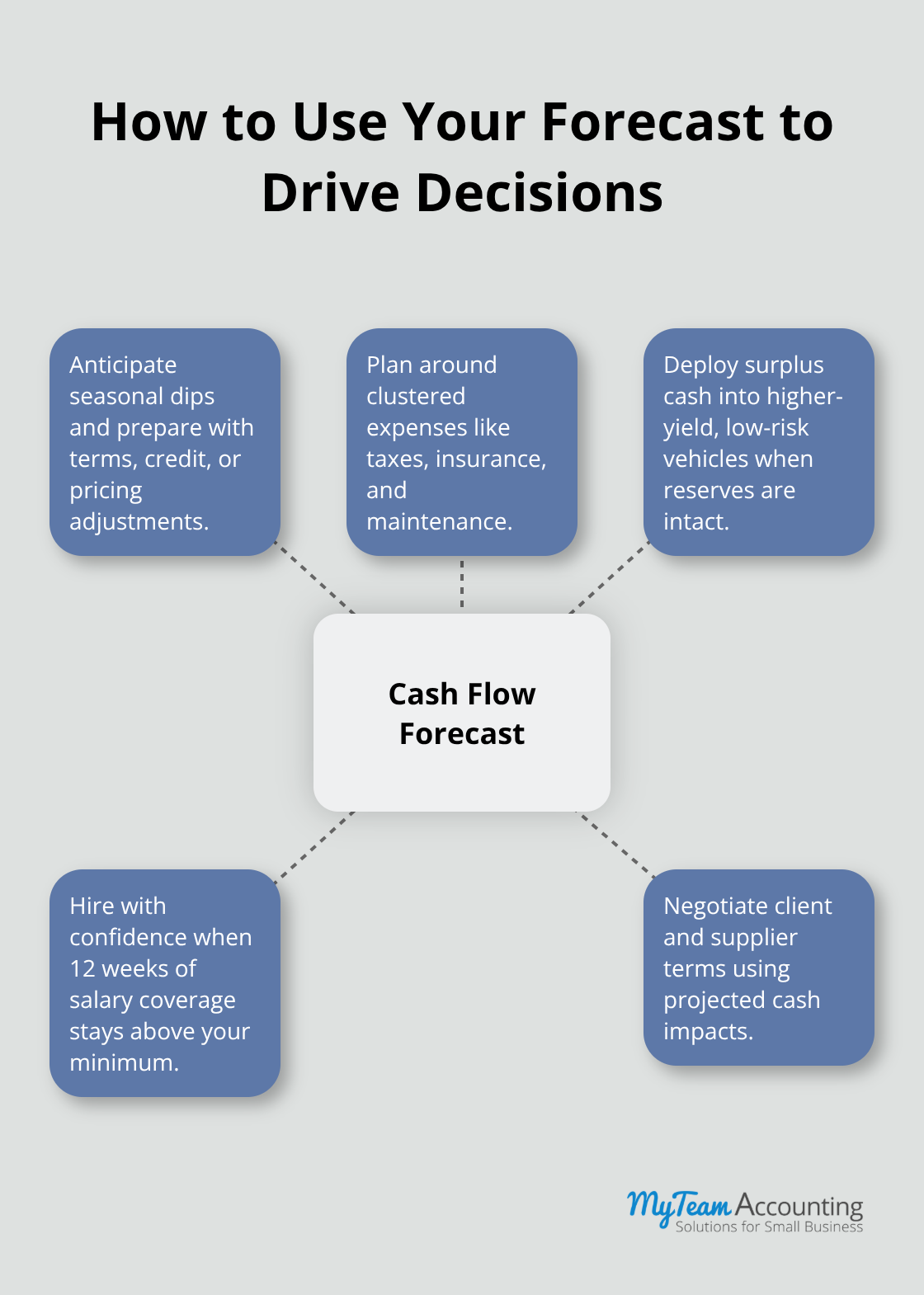

Anticipate Seasonal Patterns Before They Strike

Seasonal revenue patterns hidden in your historical data become obvious once you map them into a forward projection. If your business experiences a predictable revenue dip in July, your forecast shows this as a negative cash flow position in weeks 28 through 30. This means your accounts payable come due during your slowest revenue period. The solution isn’t to panic; it’s to act now. Negotiate extended payment terms with your three largest suppliers before July arrives. Arrange a line of credit in May when you’re cash-rich, not in July when you’re desperate. One mechanical contractor discovered through forecasting that seasonal project delays created a six-week cash crunch every March. Rather than scramble for emergency financing, they now offer clients a 3% discount for deposits on spring projects in January. This simple adjustment moved cash inflow forward by eight weeks and eliminated the annual crisis.

Your forecast also exposes where expenses cluster unexpectedly. Many businesses face quarterly tax payments, annual insurance renewals, or equipment maintenance that arrives in specific months. When you see these expenses hit your projection simultaneously with a revenue dip, you have months to prepare instead of weeks to react. Set aside the cash monthly rather than discovering in month eleven that you lack funds for the quarterly payment. This transforms what feels like a surprise into a planned expense you accumulate funds to cover.

Deploy Surplus Cash Strategically

Beyond preventing problems, your forecast identifies genuine opportunities to improve profitability that have nothing to do with increasing sales. Most owners assume profitability comes only from higher revenue. Your forecast shows otherwise. If your projection reveals that you maintain surplus cash from week six through week twelve, that capital deserves strategic deployment.

More importantly, your forecast shows exactly when you can invest in growth without creating cash stress. If your projection shows you’ll maintain at least a 90-day operating expense reserve throughout the next quarter, you have permission to invest in that equipment upgrade or marketing campaign you’ve delayed. If your forecast shows you’ll dip below your safety buffer during weeks 15 through 18, you postpone the investment until week 19. This removes emotion and guesswork from capital allocation.

Make Hiring Decisions with Confidence

The same principle applies to hiring decisions. Rather than deciding to hire based on current workload, consult your forecast. Can your cash position sustain the new salary for 12 weeks without dipping below your minimum reserve? If yes, hire now and capture the productivity gains. If no, the hire creates unnecessary risk. This discipline prevents the most common hiring mistake: bringing on staff during strong revenue periods without confirming that cash flow can sustain payroll through the inevitable slower months ahead.

Negotiate Payment Terms from a Position of Strength

Your forecast also reveals the true cost of extending payment terms to clients. If a major customer requests net-60 instead of net-30 terms, your forecast shows the exact cash impact. Rather than guessing, you see that this change extends your cash conversion cycle by 30 days, creating a temporary shortfall in week 14. You can then decide whether the relationship justifies arranging additional credit or whether you need to negotiate a compromise like net-45. This visibility transforms negotiations from reactive discussions into strategic decisions backed by data.

Final Thoughts

Cash flow forecasting is not a one-time exercise or a compliance task-it is the foundation of sustainable business growth. Businesses that thrive treat their forecast as a living document, updating it weekly with actual results and adjusting projections as conditions change. This discipline transforms financial planning from guesswork into strategy.

Start simple this week. Use a basic spreadsheet with your last 12 months of data, project the next 13 weeks conservatively, and update it every Friday. You do not need sophisticated software or perfect forecast accuracy to gain immediate value, as even a rough projection reveals when cash pressure arrives and where opportunities hide. As your business grows and your comfort with the process increases, refine your approach with scenario planning, accounting software automation, and extended forecast horizons for capital planning.

Your competitors who practice cash flow forecasting are making faster decisions, securing better financing terms, and avoiding the cash crises that derail growth. Gather your bank statements, open a spreadsheet, and project your next 13 weeks-then contact a financial advisor to discuss how professional guidance can accelerate your results. The clarity you gain will reshape how you lead your business.